Unleashing

the power

of pensions.

Pension Insurance Corporation Group Limited

Solvency and Financial Condition Report 2023

About PIC

PIC is a specialist insurer

which has become a

leader in the UK pension

risk transfer market by

focusing on our purpose:

to pay the pensions of

our current and future

policyholders.

For over a decade, PIC has been a

significant investor in areas like social

housing, renewable energy and the

UK’s universities. These investments,

which are typically sourced privately,

provide the cash flows we need to

match our liabilities at maturities

when publicly available debt is

simplynot available.

01 Directors’ Responsibility Statement

02 Report of the Independent ExternalAuditor

07 Summary

10 A. Business and performance

10 A.1 Business

11 A.2 Performance of underwriting activity

13 A.3 Performance of investment activity

13 A.4 Performance of other activities

13 A.5 Any other information

14 B. System of governance

15 B.1 Governance function

20 B.2 Fit and proper requirements

21 B.3 Risk management system including

theOwnRisk and Solvency Assessment

24 B.4 Internal control system

24 B.5 Internal Audit function

25 B.6 Actuarial function

26 B.7 Outsourcing

26 B.8 Any other information

27 C. Risk profile

28 C.1 Market risk

29 C.2 Underwriting risk

30 C.3 Operational risk

31 C.4 Expense risk

31 C.5 Credit risk

31 C.6 Liquidity risk

32 C.7 Any other information

33 D. Valuation for solvency purposes

35 D.1 Assets

38 D.2 Technical provisions

46 D.3 Other liabilities

48 D.4 Alternative methods for valuation

48 D.5 Any other information

49 E. Capital management

49 E.1 Own Funds

53 E.2 SCR and MCR

54 E.3 Use of the duration- based equity risk

submodule in the calculation of the SCR

54 E.4 Difference between the standard

formulaand any Internal Model used

56 E.5 Non-compliance with the MCR and

significant non-compliance with the SCR

56 E.6 Any other information

57 Appendix A – Glossary of terms

59 Appendix B – QRTs

Pension Insurance Corporation Group Limited is

theultimate parent Company of Pension Insurance

Corporation plc. Pension Insurance Corporation plc

isregistered in England and Wales under company

number 05706720. It is authorised by the Prudential

Regulation Authority and regulated by the Financial

Conduct Authority and Prudential Regulation Authority

(FRN 454345). Itsregistered office is at 14 Cornhill,

London EC3V 3ND.

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 2023

Directors’ Responsibility Statement

We acknowledge our responsibility for preparing the Pension

Insurance Corporation plc (the “Company” or the “Insurer”)

and Pension Insurance Corporation Group Limited (the

“Group”) Solvency and Financial Condition Report (“SFCR”)

inall material respects in accordance with the Prudential

Regulation Authority (“PRA”) Rules andthe Solvency II

Regulations.

We are satisfied that:

a) throughout the financial year in question, the insurer

andGroup have complied in all material respects with

therequirements of the PRA Rules and the Solvency II

Regulations as applicable at the level of the insurer

andGroup; and

b) it is reasonable to believe that the insurer and Group have

continued so to comply subsequently and will continue

soto comply in future.

Signed on behalf of the Board of Directors

3 April 2024

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202301

Report of the Independent External Auditor

Opinion

Except as stated below, we have audited the following

documents prepared by Pension Insurance Corporation

Group Limited and Pension Insurance Corporation,

(together‘the Entities’), as at 31 December 2023:

•

The ‘valuation for solvency purposes’ and ‘Capital

Management’ sections of the Solvency and Financial

Condition Report of the Entities as at 31 December 2023,

(‘the Narrative Disclosures subject to audit’); and

•

Group templates S.02.01, S.22.01, S.23.01, S.32.01 for the

Group, and Company templates S.02.01, S.12.01, S.22.01,

S.23.01, S.28.01 for the Company (‘the templates

subjecttoaudit’).

The Narrative Disclosures subject to audit and the templates

subject to audit are collectively referred to as the ‘Relevant

Elements of the Solvency and Financial Condition Report’.

We are not required to audit, nor have we audited, and as

aconsequence do not express an opinion on the Other

Information which comprises:

•

information contained within the Relevant Elements of the

Solvency and Financial Condition Report set out about

above which derive from the Solvency Capital

Requirement, as identified in the Appendix to this report;

•

the ‘Business and performance’, ‘System of governance’

and ‘Risk profile’ sections of the Solvency and Financial

Condition Report;

•

Group templates S.05.01 and S.25.03 for the Group;

•

Company templates S.05.01 and S.25.03 for the Company;

•

information calculated in accordance with the previous

regime used in the calculation of the transitional measure

on technical provisions, and as a consequence all

information relating to the transitional measures on

technical provisions as set out in the Appendix to this

report; and

•

elements of the Narrative Disclosures subject to audit

identified as ‘unaudited’; the written acknowledgement

bythe Directors of the Entities of their responsibilities,

including for the preparation of their relevant content

ofthe Solvency and Financial Condition Report

(‘theResponsibility Statement’).

To the extent the information subject to audit in the Relevant

Elements of the Solvency and Financial Condition Report

includes amounts that are totals, sub-totals or calculations

derived from the Other Information, we have relied without

verification on the Other Information.

In our opinion, the information subject to audit in the

Relevant Elements of the Solvency and Financial Condition

Report of the Entities as at 31 December 2023 is prepared,

inall material respects, in accordance with the financial

reporting provisions of the PRA Rules and Solvency II

Regulations on which it is based, as modified by relevant

supervisory modifications, and as supplemented by

supervisory approvals and determinations in effect as at

thedate of approval of the Solvency and Financial

ConditionReport.

Basis for opinion

We conducted our audit in accordance with International

Standards on Auditing (UK) (ISAs (UK)) including ISA (UK) 800

and ISA (UK) 805, and applicable law. Our responsibilities

under those standards are further described in the Auditor’s

Responsibilities for the Audit of the Relevant Elements of the

Solvency and Financial Condition Report section of our

report. We are independent of each of the Entities in

accordance with the ethical requirements that are relevant

to our audit of the Solvency and Financial Condition Report

in the UK, including the FRC Ethical Standard as applied to

public interest entities, and we have fulfilled our other ethical

responsibilities in accordance with these requirements. We

believe that the audit evidence we have obtained is

sufficient and appropriate to provide a basis for our opinion.

Emphasis of matter – special purpose basis

ofaccounting

We draw attention to the ‘valuation for solvency purposes’

and ‘Capital Management’ sections of the Solvency and

Financial Condition Report, which describe the basis of

accounting of the information subject to audit in the

Relevant Elements of the Solvency and Financial Condition

Report. The Solvency and Financial Condition Report is

prepared in accordance with the financial reporting

provisions of the PRA Rules and Solvency II regulations, and

therefore in accordance with a special purpose financial

reporting framework. The Solvency and Financial Condition

Report is required to be published, and intended users

include but are not limited to the Prudential Regulation

Authority. As a result, the Solvency and Financial Condition

Report may not be suitable for another purpose. Our opinion

is not modified in respect of this matter.

Report of the external independent auditor to the Directors of Pensions Insurance

Corporation Group Limited (‘the parent Company’), and Pension Insurance Corporation

pursuant to Rule 4.1 (2) of the External Audit Part of the PRA Rulebook applicable to

Solvency II firms.

REPORT ON THE AUDIT OF THE RELEVANT ELEMENTS OF THE SOLVENCY AND

FINANCIAL CONDITION REPORT

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202302

Report of the Independent External Auditor continued

Going concern

The Directors of Pension Insurance Corporation Group

Limited have prepared the information subject to audit in

the Relevant Elements of the Solvency and Financial

Condition Report for the Group on the going concern basis

as they do not intend to liquidate the Group or the parent

Company or to cease their operations, and as they have

concluded that the Group and the parent Company’s

financial positions mean that this is realistic. They have also

concluded that there are no material uncertainties that

could have cast significant doubt over their ability to

continue as a going concern for at least a year from the date

of approval of the Solvency and Financial Condition Report

(“the going concern period”). The Directors of Pension

Insurance Corporation have prepared the information

subject to audit in the Relevant Elements of the Solvency

and Financial Condition Report for their respective entity on

the going concern basis as they do not intend to liquidate

their respective entity or to cease its operations, and as they

have concluded that their respective entity’s financial

position means that this is realistic. They have also

concluded that there are no material uncertainties that

could have cast significant doubt over the ability of their

respective entity to continue as a going concern for the

goingconcern period.

We used our knowledge of the Group and Company, its

industry, and the general economic environment to identify

the inherent risks to its business model and analysed how

those risks might affect the Group and Company’s financial

resources or ability to continue operations over the going

concern period. The risks that we considered most likely to

adversely affect the Group and Company’s available

financial resources over this period were:

•

a significant deterioration in longevity experience,

potentially caused by market wide event(s);

•

a deterioration in the valuation of the Group’s investments

arising from fluctuations or negative trends in the

economic environment; and

•

the impact on regulatory capital solvency margins and

liquidity of changes in inflation and movements in foreign

exchange or interest rates.

We also considered less predictable but realistic second

order impacts such as failure of counterparties who have

transactions with the Group (such as reinsurers) to meet

commitments and a sudden and significant increase in

policyholders seeking to transfer their policies to other

providers that could give rise to a negative impact on the

Group’s financial position and increased illiquidity.

We considered whether these risks could plausibly affect

theliquidity or Solvency in the going concern period by

assessing the Directors’ sensitivities over the level of

available financial resources indicated by the Group and

Company’s financial forecasts taking account of severe, but

plausible adverse effects that could arise from these risks

individually and collectively.

Our conclusions based on this work:

•

we consider that the Directors’ of the Entities use of the

going concern basis of accounting in the preparation of

the information subject to audit in the Relevant Elements

of the Solvency and Financial Condition Report for their

respective entity and the Group is appropriate; and

•

we have not identified, and concur with the Directors’ of

the Entities assessment that there is not a material

uncertainty related to events or conditions that,

individually or collectively, may cast significant doubt on

the Entities’ or the Group’s ability to continue as a going

concern for the going concern period.

However, as we cannot predict all future events or conditions

and as subsequent events may result in outcomes that

areinconsistent with judgements that were reasonable

atthe time they were made, the above conclusions are not

aguarantee that the Entities or the Group will continue

inoperation.

Fraud and breaches of laws and regulations –

ability to detect

To identify risks of material misstatement due to fraud

(“fraud risks”) we assessed events or conditions that could

indicate an incentive or pressure to commit fraud or provide

an opportunity to commit fraud. Our risk assessment

procedures included:

•

enquiring of Directors, the audit Committee, internal audit

and inspection of policy documentation as to the Group’s

high-level policies and procedures to prevent and detect

fraud, including the Group’s channel for “whistleblowing”,

as well as whether they have knowledge of any actual,

suspected or alleged fraud;

•

reading Board, and Audit Committee minutes, Risk

Committee and Credit Rating Committee minutes; and

•

considering remuneration incentive schemes and

performance targets for management/directors.

We communicated identified fraud risks throughout the

audit team and remained alert to any indications of fraud

throughout the audit.

As required by auditing standards and taking into account

possible pressures to meet profit targets, we perform

procedures to address the risk of management override of

controls, in particular the risk that management may be in a

position to make inappropriate accounting entries and the

risk of bias in accounting estimates and judgements.

Accordingly, we identified a fraud risk related to accounting

estimates and judgements related to Best Estimate Liabilities

‘BEL’ in the valuation of technical provisions in response to

the potential for management bias.

To address the fraud risks related to management override,

we also performed procedures including identifying

journalentries and other adjustments to test based on

riskcriteria and comparing the identified entries to

supporting documentation. These included those including

specific words based on our risk criteria, those posted to

seldom used accounts and those entries containing

significant estimates posted at the end of the period

(period-end adjustments).

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202303

Report of the Independent External Auditor continued

Identifying and responding to risks of material

misstatement due to non-compliance with laws

and regulations:

We identified areas of laws and regulations that could

reasonably be expected to have a material effect on the

financial statements from our general commercial and

sector experience, and through discussion with the directors

and other management (as required by auditing standards),

and from inspection of the Group’s regulatory and legal

correspondence and discussed with the directors and other

management the policies and procedures regarding

compliance with laws and regulations.

We communicated identified laws and regulations

throughout our team and remained alert to any indications

of non-compliance throughout the audit.

The potential effect of these laws and regulations on the

financial statements varies considerably.

Firstly, the Group is subject to laws and regulations that

directly affect the financial statements including financial

reporting legislation (including related companies legislation),

distributable profits legislation, and taxation legislation and

we assessed the extent of compliance with these laws and

regulations as part of our procedures on the related financial

statement items.

Secondly, the Group is subject to many other laws and

regulations where the consequences of non-compliance

could have a material effect on amounts or disclosures in

the financial statements, for instance through the imposition

of fines or litigation. the following areas as those most likely

to have such as effect: regulatory capital and liquidity

requirements, GDPR compliance, Health and Safety

legislation, Employment and Social Security legislation,

Fraud, corruption and bribery legislation, Misrepresentation

Act, Environmental protection legislation, including emissions

trading and Climate Change Act 2008 and certain aspects of

company legislation recognising the financial and regulated

nature of the Group’s activities and its legal form. Auditing

standards limit the required audit procedures to identify

non-compliance with these laws and regulations to enquiry

of the directors and other management and inspection of

regulatory and legal correspondence, if any. Therefore, if a

breach of operation regulations is not disclosed to us or

evident from relevant correspondence, an audit will not

detect a breach.

Context of the ability of the audit to detect

fraudor breaches of law or regulation:

Owing to the inherent limitations of an audit, there is an

unavoidable risk that we may not have detected some

material misstatements in the financial statements, even

though we have properly planned and performed our audit

in accordance with auditing standards. For example, the

further removed non-compliance with laws and regulations

is from the events and transactions reflected in the financial

statements, the less likely the inherently limited procedures

required by auditing standards would identify it.

In addition, as with any audit, there remained a higher risk of

non-detection of fraud, as fraud may involve collusion,

forgery, intentional omissions, misrepresentations, or the

override of internal controls. Our audit procedures are

designed to detect material misstatement. We are not

responsible for preventing non-compliance or fraud and

cannot be expected to detect non-compliance with all laws

and regulations.

Other Information

The Directors of the Entities are responsible for their relevant

content of the Other Information.

Our opinion on the information subject to audit in the

Relevant Elements of the Solvency and Financial Condition

Report does not cover the Other Information and,

accordingly, we do not express an audit opinion or any form

of assurance conclusion thereon.

In connection with our audit of the information subject to

audit in the Relevant Elements of the Solvency and Financial

Condition Report, our responsibility is to read the Other

Information and, in doing so, consider whether the Other

Information is materially inconsistent with the information

subject to audit in the Relevant Elements of the Solvency

and Financial Condition Report, or our knowledge obtained

in the audit, or otherwise appears to be materially misstated.

If we identify such material inconsistencies or apparent

material misstatements, we are required to determine

whether there is a material misstatement in the information

subject to audit in the Relevant Elements of the Solvency

and Financial Condition Report or a material misstatement

of the Other Information. If, based on the work we have

performed, we conclude that there is a material

misstatement of this Other Information, we are required to

report that fact.

We have nothing to report in this regard.

Responsibilities of Directors of the Entities for

theSolvency and Financial Condition Report

The Directors of the Entities are responsible for the

preparation of their relevant content of the Solvency and

Financial Condition Report in accordance with the financial

reporting provisions of the PRA rules and Solvency II

regulations which have been modified by the modifications,

and supplemented by the approvals and determinations

made by the PRA under section 138A of FSMA, the PRA Rules

and Solvency II regulations on which they are based.

The Directors of the Entities are also responsible for such

internal control as they determine is necessary to enable the

preparation of their relevant content of the Solvency and

Financial Condition Report that is free from material

misstatement, whether due to fraud or error. The Directors

are responsible for assessing their respective entity’s ability

to continue as going concerns, disclosing, as applicable,

matters related to going concern; and using the going

concern basis of accounting unless they either intend to

liquidate their respective entity or to cease operations, or

have no realistic alternative but to do so.

The Directors of the parent Company are responsible for

assessing the Group’s and parent Company’s ability to

continue as going concerns, disclosing, as applicable,

matters related to going concern; and using the going

concern basis of accounting unless they either intend to

liquidate the Group or the parent Company or to cease their

operations, or have no realistic alternative but to do so.

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202304

Auditor’s Responsibilities for the audit of

theRelevant Elements of the Solvency

andFinancial Condition Report

It is our responsibility to form an independent opinion as to

whether the information subject to audit in the Relevant

Elements of the Solvency and Financial Condition Report is

prepared, in all material respects, with financial reporting

provisions of the PRA Rules and Solvency II regulations on

which it is based, as modified by relevant supervisory

modifications, and

as supplemented by supervisory

approvals and determinations.

Our objectives are to obtain reasonable assurance about

whether the information subject to audit in the Relevant

Elements of the Solvency and Financial Condition Report is

free from material misstatement, whether due to fraud or

error, and to issue an auditor’s report that includes our

opinion. Reasonable assurance is a high level of assurance,

but it is not a guarantee that an audit conducted in

accordance with ISAs (UK) will always detect a material

misstatement when it exists. Misstatements can arise from

fraud or error and are considered material if, individually

orinthe aggregate, they could reasonably be expected to

influence the decision making or the judgement of the

userstaken on the basis of the information subject to audit

inthe Relevant Elements of the Solvency and Financial

Condition Report.

A fuller description of our responsibilities is located on the

Financial Reporting Council’s website at: www.frc.org.uk/

auditorsresponsibilities.

Other Matter- Internal Model

The Company has authority to calculate the Group Solvency

Capital Requirement, and the Entities have authority to

calculate their respective entity’s Solo Solvency Capital

Requirement, using an Internal Model (the “Model”) approved

by the Prudential Regulation Authority in accordance with

the Solvency II Regulations. In forming our opinion (and in

accordance with PRA Rules), we are not required to audit the

inputs to, design of, operating effectiveness of, or outputs

from the Model, or whether the Model is being applied in

accordance with the Entities’ application or approval order.

REPORT ON OTHER LEGAL AND REGULATORY

REQUIREMENTS

Sectoral information

In our opinion, in accordance with Rule 4.2 of the External

Audit Part of the PRA Rulebook for Solvency II firms, the

sectoral information has been properly compiled in

accordance with the PRA rules and EU instruments relating

to that undertaking from information provided by members

of the Group and the relevant insurance group undertaking.

Other Information

In accordance with Rule 4.1 (3) of the External Audit Part of

the PRA Rulebook for Solvency II firms we are also required to

consider whether the Other Information is materially

inconsistent with our knowledge obtained in the audit of

each of the Entities’ statutory financial statements for the

year ended 31 December 2023. If, based on the work we

have performed, we conclude that there is a material

misstatement of this other information, we are required to

report that fact.

We have nothing to report in this regard.

This engagement is separate from the audits of the annual

financial statements of the Entities and the report here

relates only to the matters specified and does not extend to

the Entities’ annual financial statements taken as a whole.

As set out in our audit reports on those financial statements,

those audit reports are made solely to the members of the

respective Entities, as a body, in accordance with Chapter 3

of Part 16 of the Companies Act 2006. The audit work has

been undertaken so that we might state to the members of

the respective Entities those matters we are required to

state to them in an auditor’s report and for no other purpose.

To the fullest extent permitted by law, we do not accept or

assume responsibility to anyone other than the Entities and

the members, as a body, of each of the respective Entities

for the audit work, for the audit report, or for the opinions we

have formed in respect of those audits.

The purpose of our audit work and to whom we

owe ourresponsibilities

This report of the external auditor is made solely to the

Directors of the Entities, as their governing bodies, in

accordance with the requirement in Rule 4.1 (2) of the

External Audit Part of the PRA Rulebook for Solvency II firms

and the terms of our engagement. We acknowledge that the

Directors are required to submit the report to the PRA, to

enable the PRA to verify that an auditor’s report has been

commissioned by the Entities’ Directors and issued in

accordance with the requirement set out in Rule 4.1 (2) of the

External Audit Part of the PRA Rulebook for Solvency II firms

and to facilitate the discharge by the PRA of its regulatory

functions in respect of the Entities, conferred on the PRA by

or under the Financial Services and Markets Act 2000.

Our audit has been undertaken so that we might state to the

Directors those matters we are required to state to them in

an auditor’s report issued pursuant to Rule 4.1 (2) and for no

other purpose. To the fullest extent permitted by law, we do

not accept or assume responsibility to anyone other than

the Entities through their governing bodies, for our audit, for

this report, or for the opinions we have formed.

James Anderson

for and on behalf of KPMG LLP

15 Canada Square

London

E14 5GL

3 April 2024

Report of the Independent External Auditor continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202305

Report of the Independent External Auditor continued

Group

•

The following elements of Group template S.02.01.02:

•

Row R0550: Technical provisions–non-life (excluding

health) – risk margin;

•

Row R0590: Technical provisions–health (similar to

non-life) – risk margin;

•

Row R0640: Technical provisions–health (similar to life) –

risk margin;

•

Row R0680: Technical provisions–life (excluding health

and index-linked and unit- linked) – risk margin; and

•

Row R0720: Technical provisions–Index-linked and

unit-linked – risk margin.

•

The following elements of Group template S.22.01:

•

Column C0030: Impact of transitional measures on

technical provisions;

•

Row R0010: Technical provisions; and

•

Row R0090: Solvency Capital Requirement.

•

The following elements of Group template S.23.01:

•

Row R0020: Non-available called but not paid in

ordinary share capital at Group level;

•

Row R0060: Non-available subordinated mutual

member accounts at Group level;

•

Row R0080: Non-available surplus at Group level;

•

Row R0100: Non-available preference shares at Group

level;

•

Row R0120: Non-available share premium account

related to preference shares at Group level;

•

Row R0150: Non-available subordinated liabilities at

Group level;

•

Row R0170: The amount equal to the value of net

deferred tax assets not available at the Group level;

•

Row R0190: Non-available Own Funds related to other

Own Funds items approved by supervisory authority;

•

Row R0210: Non-available minority interests at Group

level;

•

Row R0380: Non-available ancillary Own Funds at Group

level;

•

Rows R0410 to R0440: Own Funds of other financial

sectors;

•

Row R0680: Group SCR;

•

Row R0740: Adjustment for restricted Own Fund items in

respect of matching adjustment portfolios and ring

fenced funds;

•

Row R0750: Other non-available Own Funds; and

•

Elements of the Narrative Disclosures subject to audit

identified as ‘unaudited’.

Company

The Relevant Elements of the Company’s Solvency and

Financial Condition Report that are not subject to audit

comprise:

•

The following elements of Solo template S.02.01:

•

Row R0550: Technical provisions–non-life (excluding

health) – risk margin;

•

Row R0590: Technical provisions–health (similar to

non-life) – risk margin;

•

Row R0640: Technical provisions–health (similar to life) –

risk margin;

•

Row R0680: Technical provisions–life (excluding health

and index-linked and unit-linked) – risk margin; and

•

Row R0720: Technical provisions – Index-linked and

unit-linked – risk margin.

•

The following elements of template S.12.01:

•

Row R0100: Technical provisions calculated as a sum of

BE and RM – risk margin; and

•

Rows R0110 to R0130: Amount of transitional measure on

technical provisions.

•

The following elements of template S.17.01:

•

Row R0280: Technical provisions calculated as a sum of

BE and RM – risk margin; and

•

Rows R0290 to R0310: Amount of transitional measure on

technical provisions.

•

The following elements of template S.22.01:

•

Column C0030: Impact of transitional measures on

technical provisions;

•

Row R0010: Technical provisions; and

•

Row R0090: Solvency Capital Requirement.

•

The following elements of template S.23.01:

•

Row R0580: SCR; and

•

Row R0740: Adjustment for restricted Own Fund items in

respect of matching adjustment portfolios and ring

fenced funds.

•

The following elements of template S.28.01:

•

Row R0310: SCR Elements of the Narrative Disclosures

subject to audit identified as ‘unaudited’.

Appendix to report of the external independent auditor to the Directors of Pension

Insurance Corporation Group Limited (‘the parent Company’) and Pension Insurance

Corporation (‘the Company’) pursuant to Rule 4.1 (2) of the external audit part of the PRA

Rulebook applicable to Solvency II firms – Relevant Elements of the Solvency and

Financial Condition Report that are not subject to audit

The Relevant Elements of the Solvency and Financial Condition Report that are not

subject to audit comprise:

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202306

The Solvency and Financial Condition Report (“SFCR”) is an annual report that is required to be produced as part of the

Solvency II (“SII”) regime in accordance with applicable Prudential Regulatory Authority (“PRA”) Rules and Solvency II

regulations. The requirement to prepare the SFCR is set out in a direction made by the PRA on 6 November 2019. Any

reference to the SII Directive in this document is a reference to the UK version of that regulation, unless otherwise stated.

The Group has permission to produce a single SFCR, covering both Pension Insurance Corporation plc (“PIC”, or the “Company”)

and Pension Insurance Corporation Group Limited (“PICG”, or the “Group”).

2022 IFRS comparatives have been restated throughout the SFCR following the Group’s adoption of IFRS 17 “Insurance

Contracts” and IFRS 9 “Financial Instruments”.

Business and performance

PIC is the primary operating subsidiary of the Group and it is authorised by the PRA to insure UK defined benefit pension

schemes. It is regulated by the PRA and the Financial Conduct Authority.

Both the Group and Company saw a decrease in their SII ratio to 211% (2022: 226% in PICGand 225% in PIC). The decrease in

the ratio in the year was primarily caused by the impact of writing £6.9 billion of new business alongside an increase in

Solvency Capital Requirement (“SCR”) from the refinement of our credit risk and hedging models. This was partly offset by

expected returns from the in-force book, the impact of risk margin reform and raising new debt, net of repurchases.

The Group IFRS profit before tax was £303 million for the year (2022: £96 million) and PIC’s profit before tax was £303 million

(2022: £96 million).

The Group also chooses to analyse its IFRS results on an alternative performance metric, Adjusted operating profit before tax

(“AOPBT”). AOPBT reflects value generated prior to the new business deferral and subsequent in-force release of profit via

the contractual service margin (“CSM”), and excludes investment related variances. The Company and Group’s AOPBT were

£893 million (2022: £383 million), an increase of 133%, largely resulting from higher expected returns reflecting higher risk-free

rates, the release of reserves following management’s review of assumptions and the greater volume of new business

written in the period.

The Group paid more than £2.1 billion, (2022: £1.8 billion) of pension payments to policyholders in 2023, with a customer

satisfaction rating of 99.3% (2022: 99.6%). Total number of pensions insured was 339,900 (2022: 302,200).

System of governance

Three lines of defence

PIC’s governance structure is in line with the “three lines of defence” model which is operated by the Group. The ‘first line’

represents the business functions who are responsible for managing risk in their day-to-day activities. The ‘second line’

consists of independent risk and compliance functions, whose responsibility is to set, monitor and oversee the risk framework

within which the first line operates, and the Actuarial Function Holder. The ‘third line’ comprises Internal Audit, which have

responsibility for assessing the operation of the risk and control environment.

The Board delegates specific responsibilities to the Board Committees, which assist the Board in its oversight and control of

the business. There are currently six Board Committees: Audit, Customer, Investment and Origination, Nomination,

Remuneration and Risk. The Investment and Origination and Customer Committees consider matters specific to PIC. The four

remaining Committees consider matters specific to both PIC and the Group, as per the delegations in their terms of

reference (further details are provided in section B.1). Members of the Committees are appointed by the Board on

recommendation of the Nomination Committee in consultation with the Committees’ chairs.

Risk Management Framework

The Risk Management Framework informs business decisions and is comprised of three elements. The first element is the risk

governance framework within which risk management responsibilities are delegated and governed. This includes the policy

framework and the implementation of three lines of defence. The second element is Risk Appetite Framework , which sets

limits and triggers in line with the Board’s risk preferences and appetite statements, within which the Group’s risk exposures

are managed. The third is the risk management system, by which risks are identified, assessed, mitigated, monitored

andreported.

Own Risk and Solvency Assessment

The annual Own Risk and Solvency Assessment (“ORSA”) assesses the risks which the Group is currently exposed to and the

forward-looking risks to the successful execution of the Group’s business strategy and objectives over the planning horizon.

This includes risks to all elements of the Group’s Risk Appetite Framework, including quantifiable risks such as solvency and

liquidity, and non-quantifiable risks such as conduct and reputational.

The ORSA provides an ongoing process to identify, assess, monitor and manage the most material risks to PIC’s business plan

and solvency over both the near term and the five-year business planning horizon.

Risk Profile

The Group and Company quantify their exposure to different types of risk using their Internal Model, which was approved for

use by the PRA in December 2015.

Summary (unaudited)

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202307

The Group’s total SCR represents the amount of capital the firm must hold to protect itfrom extreme risk events and comply

with regulatory requirements. The component risks which make up the SCR are detailed in section C.

The Group’s risk profile has remained stable over the reporting period.

Valuation for solvency purposes

The table below summarises the Group and Company’s assets and liabilities valued in accordance with its statutory

accounting basis (IFRS), and the Solvency II regulatory basis at 31 December:

2023

Group Company

Solvency

£m

IFRS

£m

Solvency

£m

IFRS

£m

Total Assets 78,438 78,538 78,347 78,441

Total Liabilities 71,855 74,070 71,806 73,992

Excess of Assets over Liabilities/Equity 6,583 4,468 6,541 4,449

2022

Group Company

Solvency

£m

IFRS

£m

(Restated*)

Solvency

£m

IFRS

£m

(Restated*)

Total Assets 65,461 65,225 65,429 65,191

Total Liabilities 59,582 60,850 59,596 60,848

Excess of Assets over Liabilities/Equity 5,879 4,375 5,833 4,343

* 31 December 2022 comparatives have been restated following the Group’s adoption of IFRS 9 “Financial Instruments” and IFRS 17

“Insurance Contracts”.

Differences in the valuation of assets and liabilities between the two bases are driven primarily by the following:

•

valuation of best estimate liabilities under Solvency II is higher than under IFRS, mainly due to differences in discount rates;

•

the Solvency II risk margin (net of transitional measures for technical provisions (“TMTP”)) which is an addition to the

Solvency II best estimate liabilities but is not required under IFRS;

•

IFRS 17 risk adjustment for non-financial risk is included in the IFRS 17 insurance and reinsurance balances which represents

the compensation PIC requires for taking non-financial risk (predominantly longevity and expense risk);

•

IFRS 17 contractual service margin which represents the unearned profit that the Group will recognise as it provides

insurance contract services;

•

valuation of subordinated debt liabilities, which are at amortised cost for IFRS purposes and at fair value under Solvency II;

and

•

deferred tax on the above.

The valuation differences above are explained in greater detail in section D.

Summary (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202308

Capital management

At 31 December 2023, PIC and the Group’s Solvency II ratios were 211% (2022: PIC 225%; PICG 226%) and they had surplus funds

of£4,320 million and £4,331 million respectively (2022: PIC £4,011 million; PICG £4,037 million) in excess of their SCR. The decrease

in the ratios in the year were primarily caused by the impact of writing £6.9 billion of new business alongside an increase in SCR

from the refinement of our hedging and credit risk models. This was partly offset by expected returns from the in-force book,

the impact of risk margin reform and raising new debt, net of repurchases.

On 13 November 2023, PIC issued £500 million subordinated loan notes, maturing in 2033, with a fixed coupon of 8.0% paid

annually in arrears. These notes were issued at 99.7% of par. Following the issue, £97 million of the 2024 and £203 million of the

2026 loan notes were repurchased for a total cost of £310 million.

On 26 March 2024, the Board approved a final dividend for 2023 of £147 million (2022: £100 million).

The Group’s dividend policy is to retain sufficient capital to invest in future growth opportunities of the UK pension risk

transfer market, whilst paying regular dividends to shareholders, based on the current and future projected capital position

of the business. The implications for solvency, leverage and liquidity are all considered when considering the appropriateness

of dividend payments.

The table below summarises the Group and Company’s capital and solvency position as at 31 December:

2023 Group Company

Own Funds £m 8,221 8,210

SCR £m 3,890 3,890

Solvency II surplus £m 4,331 4,320

Solvency II ratio % 211% 211%

2022 Group Company

Own Funds £m 7,236 7,210

SCR £m 3,19 9 3,19 9

Solvency II surplus £m 4,037 4,011

Solvency II ratio % 226% 225%

Summary (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202309

A.1 Business

A.1.1 Business overview

The full legal name of the undertaking is Pension Insurance Corporation plc. It is a Public Limited Company, registered

inEngland and Wales with the company registration number 05706720.

PIC is authorised by the Prudential Regulation Authority, 20 Moorgate, London EC2R 6DA and regulated by the Financial

Conduct Authority, 12 Endeavour Square, London E20 1JN and the Prudential Regulation Authority (FRN 454345).

The principal activity of PIC is the provision of pension risk transfer contracts to corporate pension schemes (also known as

“pension insurance” or “bulk annuities”). Pension risk transfer products are used by pension funds to transfer the risks and

liabilities arising from the benefit promises made to pension fund members to an insurance company.Insurance is also used

as a means by which the ultimate responsibility to pay the benefits promised is transferred to the insurance company

through the issuance of an individual annuity insurance policy to the pension fund member.

A.1.2 Legal structure of the Group

A simplified Group structure chart and a description of the Group as at 31 December 2023 are set out below:

Pension Insurance Corporation Group Limited (“PICG”)

PIC Holdings Limited (“PICH”)

Pension Services

Corporation Limited (“PSC”)

Pension Insurance

Corporation plc (“PIC”)

Group undertakings

Country of

incorporation Principal activity

Pension Insurance Corporation

GroupLimited

England Holding company for the other companies within the Group,

owning 100% of the equity. It has no employees and incurs

minimal administrative expenses. It also operates share

incentive plans for the benefit of the employees of the Group.

PIC Holdings Limited England An intermediate holding company, and has no material assets

or liabilities in the context of the Group.

Pension Insurance Corporation plc

(Regulated entity)

England Provision of insurance annuity products to corporate pension

schemes and their members. It also issues Restricted Tier 1 notes

and Tier 2 subordinated debt.

Pension Services Corporation Limited England Service company of the Group, and employs all the staff which are

responsible for the performance of the Group’s activities. It also

enters into the majority of material contracts (with the exception

of pension insurance contracts) on behalf of the Group.

The Group and Company prepare their financial statements in accordance with IFRS in conformity with the requirements

ofthe Companies Act 2006. There are no differences between the scope of the Group for the consolidated financial

statements and the scope under the default accounting consolidation method for solvency purposes. The external

auditorto the Group is KPMG LLP, 15 Canada Square, London E14 5GL.

A.1.3 Significant events in the period

Key appointments (Board level)

The following changes were made to the Board of Directors of PICG between 1 January 2023 and the date of this report:

Mark Stephen stepped down from the Board on 31 December 2023 and Andy Moss was appointed on 1 January 2024.

The following changes were made to the Board of Directors of PIC between 1 January 2023 and the date of this report:

Mark Stephen stepped down on 31 December 2023 and Andy Moss was appointed on 1 September 2023.

Arno Kitts was appointed the Board Sustainability Champion effective from 6 October 2023.

A. Business and Performance (unaudited)

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202310

Other key transactions

On 26 March 2024, the Board approved a final dividend for 2023 of £147 million (2022: £100 million).

Key business transactions

PIC has completed the £6.2 billion buy-in of two schemes sponsored by RSA Group, covering c.40,000 members. Following

this transaction, our balance sheet has remained very strong with a solvency ratio at 31 December 2023 of 211% (2022: 225%).

This positions us well to fulfil our purpose of paying the pensions of our current and future policyholders, as well as helping the

trustees of defined benefit schemes to secure the pension benefits of their members.

Transition to IFRS 17 reporting

From 1 January 2023, the Group adopted IFRS 17 “Insurance Contracts”, the new global insurance accounting standard that

has fundamentally changed how companies account for insurance and reinsurance contracts, including measurement,

income statement presentation and disclosure.

A.2 Performance of underwriting activity

The PIC and Group’s profit before tax for year was £303 million (2022: PIC £96 million; PICG £96 million).

In addition to the statutory result above, the Group also chooses to analyse its IFRS results using an alternative performance

metric, AOPBT, which has been redefined following the Group’s adoption of IFRS 17. The Group considers this alternative

performance metric to be an important metric for stakeholders as it reflects the Group’s operating activities which are core to

our business alongside certain management choices and decisions around those activities. This includes the writing and

management of pension insurance contracts and the management of risk through reinsurance. The operating performance of

the Group includes the full value generated from writing new business prior to the new business deferral and subsequent

in-force release of profit via the CSM, and excludes investment related variances. AOPBT for the period, for both PIC and the

Group, increased by 133% to £893 million (2022: PIC £383 million; PICG £383 million ), largely resulting from higher expected returns

reflecting higher risk-free rates, the release of reserves following management’s review of assumptions and the greater volume

of new business written in the period.

Information on premiums, claims and changes in technical provisions, which can be considered as key elements of underwriting

performance, is presented by Solvency II line of business in Quantitative Reporting Template (“QRT”) S.05.01 inAppendix B of

this report.

Adjusted operating profit before tax

2023 2022

Group

£m

Company

£m

Group

£m

(restated*)

Company

£m

(restated*)

Expected return from operations 495 495 264 264

New business and reinsurance profit 444 444 329 329

Underlying profit 939 939 593 593

Changes in valuation assumptions 194 194 12 12

Experience and other variances (18) (18) (19) (19)

Finance, project and other costs (222) (222) (203) (203)

Adjusted operating profit before tax 893 893 383 383

Movement in CSM (585) (585) (409) (409)

Investment related variances (38) (38) 89 89

Add back: Restricted Tier 1 coupon (treated as a dividend for statutory

purposes) 33 33 33 33

Profit before taxation 303 303 96 96

* 31 December 2022 comparatives have been restated following the Group’s adoption of IFRS 17 “Insurance Contracts”.

A.2.1 Underlying profit

Underlying profit has increased to £939 million (2022: £593 million). This includes:

•

Expected return from operations reflects the long-term expected returns arising from the management of the Group’s

assets and liabilities. It is based on opening economic assumptions applied to the opening assets and liabilities. Expected

returns of £495 million were above the prior year (2022: £264 million), mainly driven by the increase in opening interest rates.

A. Business and Performance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202311

•

New business and reinsurance profit represents the impact on profit of writing new pension risk transfer contracts and the

impact of entering into new reinsurance contracts on the in-force book. The profit is calculated using the economics at the

initial recognition date, the locked-in liquidity premium, expected reinsurance, pricing demographic and expense

assumptions and the target asset portfolio mix assumptions. New business also includes any acquisition expense variance,

being the difference between the actual acquisition expenses incurred in the year and those used in pricing. Any premium

adjustments or deferred acquisition costs are also included in this line.

New business andreinsurance profit was £444 million (2022: £329 million), resulting from the £6.9 billion of new business

premiums written (2022: £4.1 billion), primarily driven by the RSA transaction.

A.2.2 Changes in valuation assumptions

The Group’s focus remains on long-term profitability, and so we set assumptions in respect of the in-force liabilities and new

business acquired during the year, using our best estimate and applying an adjustment for non-financial risk. Under IFRS 17,

the impact of changes in such items is added to the CSM and spread over the future expected duration of the contracts.

AOPBT is shown before this deferral. Management regularly review these assumptions to ensure that they reflect the

characteristics of the Group’s book and wider market practice.

As part of this review in 2023, updated assumptions resulted in a benefit to AOPBT of £194 million (2022: £12 million).

A.2.3 Experience and other variances

Experience and other variances gave rise to a loss of £18 million in 2023 for both PICG and PIC (2022: PICG and PIC loss of

£19 million). Favourable impacts from updates to policy data were offset by differences between the maintenance expense

assumptions used for pricing new business compared to those used in the valuation basis; this negative expense variance

was partly offset by a reserve release within changes in valuation assumptions.

A.2.4 Finance, project and other costs

The interest costs of the subordinated Tier 2 debt capital issued by PIC and transaction costs increased slightly to £91 million

in 2023 (PICG: £91 million) from £90 million the previous year (PICG: £90 million).

Interest coupons paid on the Restricted Tier 1 (“RT1”) debt issued by PIC were £33 million (PICG: £33 million) and were unchanged

from prior year.

Project and other costs in 2023 were £98 million (PICG: £98 million) compared with costs of £80 million (PICG: £80 million) inthe

prior year. They reflect costs associated with other business-wide initiatives, alongside other shareholder and

regulatorycosts.

A.2.5 Movement in CSM

The movement in CSM comprises the deferral of new business profits on contracts written in the year and interest accretion

on the opening CSM, alongside the impact of changes in non-financial assumptions and experience variances on the CSM,

partly offset by the amortisation of CSM in respect of in-force business.

During the year, the total increase in CSM was £585 million, net of reinsurance (2022: £409 million). The CSM recognised from

new business written in year was £337 million up from £317 million in 2022. This reflects the new business written in the year

and represents an increase in the store of future value and the growth in the business. The amortisation of CSM also

increased to £181 million from £133 million in 2022 reflecting the increase in the size of the in-force book.

A.2.6 Investment related variances

Investment related variances include the differences between the expected long-term investment return and the actual

investment return earned in the period; changes in economic assumptions on liabilities and the impact of changes in

creditratings.

The Group carefully manages its risk to market and other economic factors and enters into derivative hedging contracts

tomanage these exposures in accordance with its risk appetite. The Group’s hedging strategy is primarily designed to

actively manage risk over the long term in the solvency balance sheet, and there exists a mismatch between this hedging

strategy and the IFRS balance sheet. This mismatch, and the resulting volatility, is included within the investment related

variance line.

Investment related variances resulted in a loss of £38 million in the period (2022: gain of £89 million), largely driven by

movements in interest rates and credit spreads partly offset by asset optimisation activities. In the prior year, the benefit

predominantly related to favourable market movements, including inflation movements and credit spreads.

A.2.7 Other operational highlights

In 2023, PIC was responsible for the current and future pension payments of 339,900 (2022: 302,200) policyholders. This includes

those with individual policies, and those for whom the trustees of the underlying pension schemes retain ultimateresponsibility.

At 31 December 2023, 85% (2022: 87%) of the Group’s gross benefit reserves had been reinsured. The Group has 14 reinsurance

counterparties, all of which have a credit rating of A- or above.

A. Business and Performance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202312

A.3 Performance of investment activity

The investment performance (including commissions earned) presented in the table below is a reflection of income,

gains(realised and unrealised), losses and expenses arising from the investment portfolios owned by the Group.

Investment return: by Solvency II asset class

Group and Company

2023

£m

2022

£m

(restated*)

Government bonds 549 (5,740)

Corporate bonds 1,218 (3,899)

Collective investment undertakings 85 293

Cash and deposits 12 12

Collateralised securities 27 (52)

Mortgages and loans 575 (3,1 97 )

Derivative-based instruments 743 224

Commissions earned 1 1

Investment return 3,210 (12,358)

Investment management expenses (54) (50)

Total 3,156 (12,408)

* 31 December 2022 comparatives have been restated following the Group’s adoption of IFRS 9 “Financial Instruments”.

Investment return comprises income received on fixed income securities, derivatives and investment property, and

unrealised and realised gains and losses on these investments. The table above allocates investment return across

theSolvency IIasset classes.

A.3.1 Gains and losses recognised directly in equity

Consistent with prior year, the Group did not recognise any gains or losses related to the Group’s investments directly in

equity during the year.

A.3.2 Information on securitisation

PIC invests in equity release mortgages (“ERMs”) because they are a good match for its long-term liabilities, and help diversify

the portfolio. ERMs are loans secured against property that are repayable on death or entry into long-term care of the

borrower. An ERM can also be repaid early voluntarily by the borrower, in which case an early repayment charge may apply.

The majority of PIC’s portfolio of ERMs has been legally transferred to the Group’s subsidiary PIC ERM 1 Limited; however PIC

retains substantially all of the risks and rewards of ownership through its holding of loan notes issued by PIC ERM 1 Limited.

The market value of securitised ERMs at 2023 was £1,110 million (2022: £887 million).

A.4 Performance of other activities

The Group does not have any other material activities.

A.5 Any other information

Economic uncertainty and market volatility

The global economic outlook continued to be volatile in 2023, with fluctuating interest rates and growing geopolitical risks,

particularly the continued Russian invasion of Ukraine and the conflict between Israel and Hamas.

The impacts of these market conditions on PIC can be both positive and negative. The current market conditions have

resulted in higher risk of credit downgrades and defaults, and heightened risk overall. Sustained levels of downgrades and

defaults would impact PIC’s solvency position. However, higher yields without downgrades or defaults could improve PIC’s

solvency position. The Group constantly monitors market conditions and has risk appetite limits for PIC’s exposure to market

risks. PIC also holds sufficient capital to protect the business against market movements and downgrades and defaults, and

it continues to develop its methodology for calculating the amount of capital to hold.

Rounding convention

The SFCR is presented in pounds sterling rounded to the nearest million which is consistent with the presentation in the IFRS

financial statements. The QRTs are presented in pounds sterling rounded to the pound. Rounding differences of +/- one unit

can occur.

A. Business and Performance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202313

B. System of Governance (unaudited)

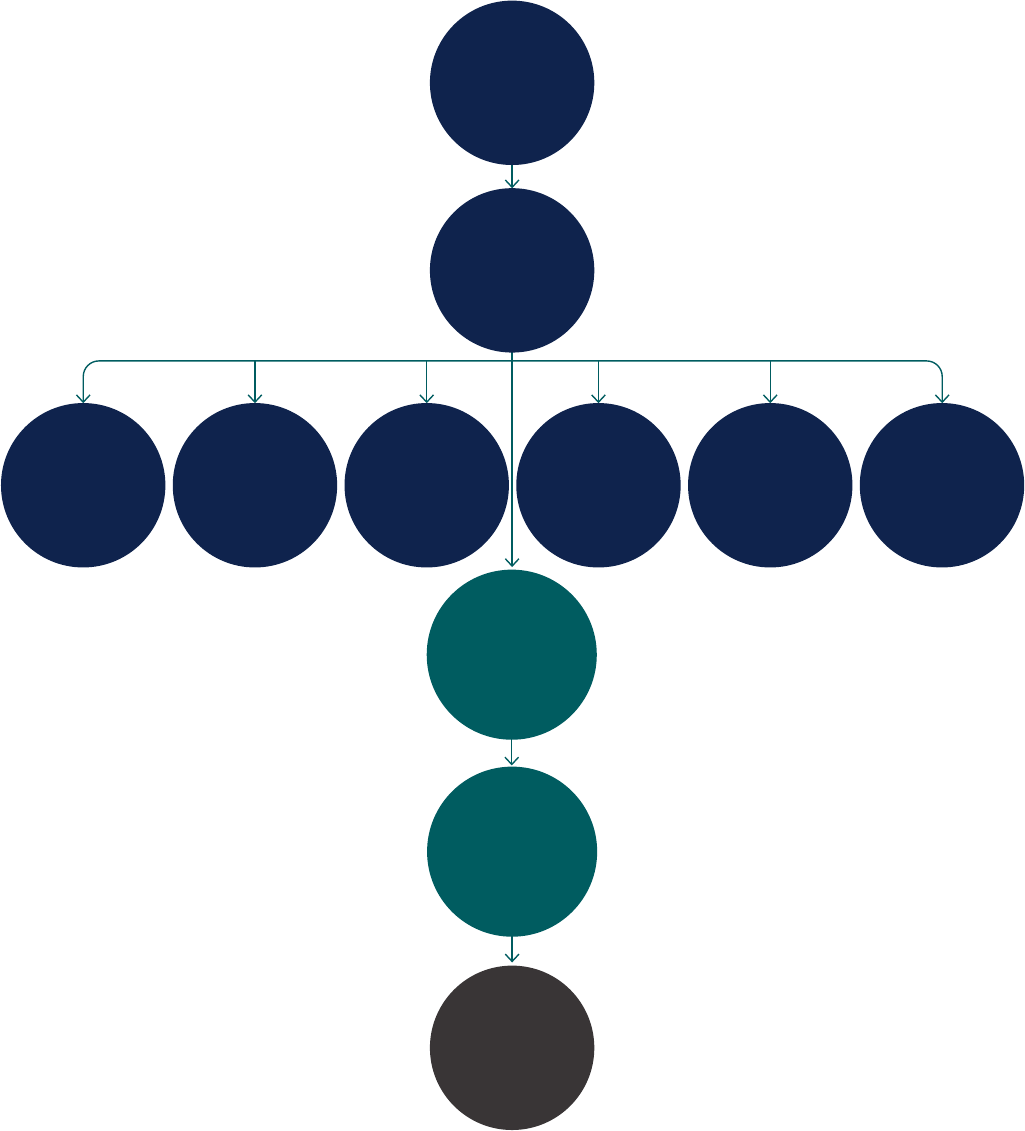

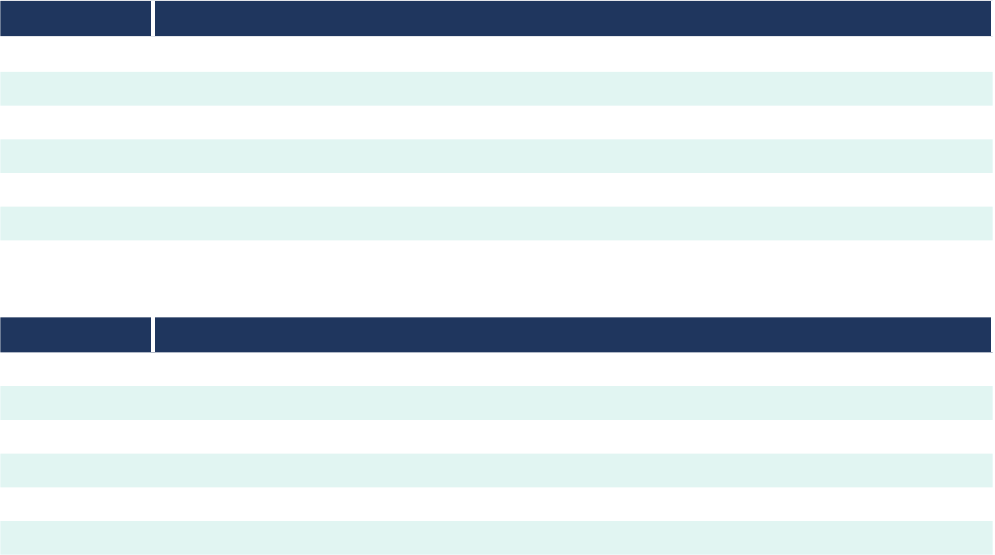

The below chart shows the Group’s governance structure. Along with other annual reviews of our governance processes, the

structure is reviewed to make sure that it is fit for purpose and remains as such in the context of the Group’s growthprospects.

PICG

Board

Executive

Committee

Chief

Executive

Officer

Investment

and Origination

Committee

Board

Customer

Committee

Nomination

Committee

Remuneration

Committee

Risk

Committee

Audit

Committee

Management

and Operating

Committees

PIC

Board

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202314

B.1 Governance function

B.1.1 Board of Directors

Pension Insurance Corporation Group Limited

PICG is governed by its Board consisting of 13 Directors, 12 of whom are non-executive.

Of the non-executive Board members: two are nominated by Reinet PC Investments (Jersey) Limited, which as at 31 December 2023

holds a 49.496% interest in PICG; one is nominated by Luxinva S.A., a wholly owned subsidiary of the AbuDhabi Investment

Authority, which holds a 18.416% interest in PICG; one is nominated by Blue Grass Holdings Limited, aCVC entity, which holds a

17.376% interest in PICG; and one is nominated by MP 2019 K2 Aggregator, L.P., an HPS Investment Partners entity, which holds

a 10.231% interest in PICG.

The Board maintains overall responsibility for PICG Limited as an entity and an oversight responsibility for the Group to

ensure the Group operates in the best interests of its policyholders, shareholders, employees and other stakeholders.

TheBoard is also responsible for setting the Group’s long-term objectives and commercial strategy.

The main activities of the Group are conducted through its principal operating subsidiary, PIC.

The Board has delegated the day-to-day management and administration of the Company to the Chief Executive Officer

(“CEO”) who has established the Executive Committee at the operating entity level, PIC, to assist the CEO in the day-to-day

running of PIC.

Pension Insurance Corporation plc

PIC is governed by its Board consisting of 15 Directors until 31 December 2023 (14 Directors from 1 January 2024), 12 of whom are

non-executive.

Of the non-executive Board members: one is appointed by Reinet PC Investments (Jersey) Limited, one is appointed by LuxinvaS.A.,

a wholly owned subsidiary of the Abu Dhabi Investment Authority; one is appointed by Blue Grass Holdings Limited, a CVC

entity; and one is nominated by MP 2019 K2 Aggregator, L.P., a HPS Investment Partners entity.

Pension Insurance Corporation plc is a wholly owned subsidiary of PIC Holdings Limited which is a wholly owned subsidiary of

the ultimate parent entity Pension Insurance Corporation Group Limited.

The Board has overall responsibility for the operations of PIC and oversees the management of the Company in the best

interests of its policyholders, shareholders, employees and other stakeholders, and sets the Company’s long-term objectives

and commercial strategy.

The Board has delegated responsibility for a number of functions to Board Committees as set out below. The Committees

allhave terms of reference setting out their responsibilities in more detail.

B.1.2 Audit Committee

The Board has established the Committee in fulfilling its responsibilities regarding financial reporting, sustainability reporting

including Task Force on Climate-related Financial Disclosures report, the effectiveness ofinternal control and risk

management systems, processes and compliance matters.

The Audit Committee comprises four independent Non-Executive Directors. The Board is satisfied that members of the

AuditCommittee have relevant accounting and financial reporting experience.

The Board has delegated the responsibility of overseeing the following key areas to the Committee:

Financial and non-financial reporting

The Audit Committee monitors and, where necessary, challenges the Group’s financial reporting processes including key

accounting issues andjudgements as well as methods and assumptions used in the valuation of the technical provisions

under Solvency II andunder IFRS.

The Committee reviews and, where necessary, challenges all material information presented in the Annual Report and

Accounts and Sustainability Report before these are approved by the Board, and approves the Task Force on Climate-

related Financial Disclosures report.

The Committee is also responsible for reviewing the Group’s assessments of going concern, longer-term prospects and

viability of the business, and reviews of anyapplicable material which the Committee is required to review under the Group’s

and the Company’s Reporting and Disclosure Policy.

Internal controls and risk management

The Audit Committee oversees, reviews, challenges and assesses the framework, effectiveness and adequacy of the Group’s

systems of internal controls, including key financial, operational and compliance controls. The Committee also reviews whether

management has discharged its duty to maintain the effectiveness of such systems, processes and controls. The Committee

meets regularly with management, the Chief Risk Officer, the General Counsel and the Chief Internal Audit Officer to ensure

management take action to address any issues arising from this review.

B. System of Governance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202315

The Committee reviews and approves the statements to be included in the annual report concerning the effectiveness of the

internal controls and risk management.

The Committee also oversees the annual validation process of the regulatory balance sheet and, jointly with the Risk

Committee, making appropriate recommendations to the Board.

The Audit Committee liaises closely with the Risk Committee to identify and mitigate any significant risk to the Group,.

Compliance, financial crime and whistleblowing

The Audit Committee reviews the Group’s compliance policies and procedures as part of oversight of the Group’s

compliance, with relevant regulatory and legal requirements, including the arrangements in place for the reporting and

investigation of concerns andfor ensuring fair customer outcomes.

The Committee reviews the adequacy of the Group’s whistleblowing policies and procedures, ensuring that such

arrangements allow for proportionate and independent investigation of such matters, and appropriate follow-up actions.

Reviewing the Group’s procedures for detecting fraud, systems and controls for prevention of bribery and market abuse is

also a function of the Committee.

Internal and External Audit

The Audit Committee oversees and monitors the role and effectiveness of the Group’s Internal Audit Function including approving

the annual internal audit plan, monitoring the reports arising from internal audits and the status of actions resulting therefrom.

The appointment or removal of the Chief Internal Audit Officer is also a key function of the Audit Committee.

The Committee is also responsible for reviewing and approving the integrated assurance plan, ensuring it aligns with the key

risks of the business.

The Committee manages the relationship with the external auditor; monitoring and reviewing its independence, objectivity and

performance, and leading any processes regarding audit tender or Senior Statutory Auditor change.

The Committee considers and makes recommendations to the Board on the appointment of the external auditor (including

approving theremuneration and terms of appointment) as well as reviewing the external auditor’s annual audit programme

and the resultstherefrom. It also reviews the policy on non-audit services carried out by the external auditor.

KPMG has been the external auditor for the Group for the last 17 years, with a tendering process last completed in 2016.

TheCommittee has taken due regard of the current Audit Directive and FRC guidance in respect of audit tendering. The

Committee approved the rotation of auditors from 1 January 2026, as required, meaning KPMG will perform its final audit for

the full year 2025 financial statements. The Committee has proactively started engagement with prospective audit firms as

part of its preparations.

B.1.3 Risk Committee

The Risk Committee provides oversight and advice to the Board on the current and future risk exposure of the Group

including oversight of the future risk strategy; determination of risk appetite and tolerance; and internal controls required

tomanage risk and the effectiveness of the Risk Management Framework. The Risk Committee oversees the operation and

development of the Internal Model.

The Committee comprises six Non-Executive Directors, five of whom are regarded as independent and the remaining

Director is shareholder nominated.

The Board has delegated to the Committee the responsibility for overseeing the following key areas:

Risk strategy, appetite and policies

The Risk Committee advises the Board on the Company’s overall risk exposures, and the current and future risk strategy.

TheCommittee reviews and recommends the Company’s design and implementation of Risk Management Framework

andmeasurement strategies to the Board. It ensures that climate change risks are appropriately incorporated in the Risk

Management Framework and the risk strategy. The Committee also reviews the risk appetite and tolerances and

recommends these to the Board for approval.

Risk oversight and monitoring

The Risk Committee monitors the Company’s overall risk identification, assessment and management process that influence

the Board’s decision making. The Committee is responsible for the oversight of Internal Model and reporting totheBoard on any

areas needing improvement, as well as updating the Board on the status of efforts to improve previously identified weaknesses.

The Committee advises the Board on the risks to the business plan and capital implications making sure that these are

adequately identified and assessed as part of the business planning process through stress testing and scenario analysis.

The Committee also works with the Nomination and Remuneration Committee to ensure that risk management is taken into

consideration in objective setting and the design of overall remuneration and risk weightings are applied to performance

objectives. It further provides advice, oversight and challenge necessary to embed and maintain a supportive risk culture

throughout the Company.

B. System of Governance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202316

The Risk Committee also reviews reports on any material breaches of risk and compliance limits and material incidents.

TheCommittee monitors the adequacy of proposed actions and management’s responsiveness to remedial actions.

Public and regulatory disclosures

The Risk Committee reviews and recommends any risk related public and regulatory disclosures to the Board, such as the

Company’s ORSA reports, processes and outputs.

Risk Function and the Chief Risk Officer

The Risk Committee considers and approves the Risk Function and Actuarial Function Mandate and reviews and assesses

performance of the Chief Risk Officer (“CRO”). It works with the Nomination Committee on making recommendations to the

Board with regard to the appointment and removal of the CRO.

B.1.4 Investment and Origination Committee

The Investment and Origination Committee is responsible for overseeing the management of the investment policy and

investment strategy for PIC, and to provide oversight of the operation of PIC’s investment portfolios within the strategic and

risk frameworks. The Committee plays a key role in PIC’s governance of pricing by providing oversight of portfolio pricing for

large deals. The Committee is responsible for overseeing the integration of environmental, social and governance risks

(including climate change) into its decision making process and within the investment policy and for reviewing management’s

proposals on the Group’s sustainability strategy as it relates to PIC’s investments and their impact on asset holdings, third

parties and investment partners in line with risk strategy, appetite and limits.

The Committee also oversees all aspects of PIC’s new business and reinsurance origination within established strategy,

business plan and risk frameworks including conduct risk.

The Committee approves the pricing assumptions at least annually and approves the pricing authority for management.

The Committee comprises seven Non-Executive Directors, three of whom are regarded as independent and the remaining

four Directors are shareholder nominated.

B.1.5 Nomination Committee

The role of the Nomination Committee is to regularly review the structure, size and composition (including the skills,

knowledge, experience and diversity) of the Board and the Executive Committee, and to make recommendations

totheBoard with regard to any changes.

The Committee also oversees the process by which the Board and its Committee, with input from individual directors, assess

their performance; and reviews the results of this evaluation and makes appropriate recommendations to the Board.

The Committee comprises five Non-Executive Directors, three of whom are regarded as independent and the remaining two

Directors are shareholder nominated.

B.1.6 Remuneration Committee

The role of the Remuneration Committee is to determine and agree with the Board the framework or broad policy for the

remuneration of all employees and the specific compensation in respect of the Company’s Chairman, Non-Executive

Directors, Chief Executive, Executive Directors, Executive Committee and other material risk takers.

In 2023, the Committee expanded its remit to cover other people related matters. This includes assisting the Board in its

overall responsibility for overseeing the development and measuring of the Group’s culture, monitoring the Group’s diversity

and inclusion initiatives, employee engagement and general capacity and capability.

The Committee comprises six Non-Executive Directors, four of whom are regarded as independent and the remaining two

Directors are shareholder nominated.

B.1.7 Board Customer Committee

The role of the Board Customer Committee is to provide oversight and advice to the Board in relation to the implementation,

prioritisation, delivery and embedding of the new Consumer Duty requirements in the Company’s processes and business

activities. The Committee will also provide an annual customer satisfaction report to the Board.

The Committee comprises three independent Non-Executive Directors.

B.1.8 Environmental, Social and Governance (“ESG”) Committee

The ESG Committee was in place until 29 June 2023 when it was disbanded and its activities were reallocated to the other

Board Committees as part of embedding ESG into the Board and Committee structure. The ESG Committee met in March

and June 2023. The purpose of the Committee was to consider and oversee all ESG related matters and to ensure that the

Board and its Committees provide oversight of the Group’s ESG strategy and activities and that the Group complies with

legal and regulatory requirements in respect of ESG, enabling the Group to make the right decisions for the long-term benefit

ofits policyholders.

B. System of Governance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202317

B.1.9 Executive Committee

The Executive Committee consists of the CEO, Chief Financial Officer (“CFO”) and senior management of the Company. Its role

is to assist the CEO in the overall management of the Company including (but not limited to) proposing strategy to the Board

and, once approved, implementing it together with operational plans, policies, procedures and budgets. The Committee’s

purpose is also to shape, embed and maintain a culture which safeguards PIC’s values by promoting attitudes and behaviours