Creating

long-term

social value.

Pension Insurance CorporationGroup Limited

Solvency and Financial Condition Report 2021

About PIC

PIC is a specialist insurer which has

become a leader in the UK pension

risk transfer market by focusing on

our purpose: to pay the pensions of

our current and future policyholders.

We aim to balance the interests of all

our stakeholders – policyholders,

employees, shareholders, regulators

and others – with excellence in

customer service at the heart of

what we do.

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 2021

01 Directors’ Responsibility Statement

02 Report of the Independent ExternalAuditor

07 Summary

13 A. Business and performance

13 A.1 Business

14 A.2 Performance of underwriting activity

16 A.3 Performance of investment activity

16 A.4 Performance of other activities

17 A.5 Any other information

18 B. System of governance

19 B.1 Governance Function

25 B.2 Fit and proper requirements

26 B.3 Risk management system including the Own

Risk and Solvency Assessment

28 B.4 Internal control system

30 B.5 Internal audit function

31 B.6 Actuarial function

32 B.7 Outsourcing

32 B.8 Any other information

33 C. Risk profile

33 C.1 Market risk

34 C.2 Underwriting risk

35 C.3 Operational risk

35 C.4 Expense risk

35 C.5 Credit risk

36 C.6 Liquidity risk

36 C.7 Any other information

37 D. Valuation for solvency purposes

39 D.1 Assets

42 D.2 Technical provisions

50 D.3 Other liabilities

51 D.4 Alternative methods for valuation

52 D.5 Any other information

53 E. Capital management

53 E.1 Own Funds

56 E.2 SCR and MCR

57 E.3 Use of the duration- based equity risk sub

module in the calculation of the SCR

57 E.4 Difference between the standard formula

and any internal model used

58 E.5 Non-compliance with the MCR and

significant non-compliance with the SCR

58 E.6 Any other information

59 Appendix A – Glossary of terms

61 Appendix B – QRTs

Pension Insurance Corporation Group Limited is

theultimate parent company of Pension Insurance

Corporation plc. Pension Insurance Corporation plc

isregistered in England and Wales under company

number 05706720. It is authorised by the Prudential

Regulation Authority and regulated by the Financial

Conduct Authority and Prudential Regulation Authority

(FRN 454345). Itsregistered office is at 14 Cornhill,

London EC3V 3ND

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202101

Directors’ Responsibility Statement

We acknowledge our responsibility for preparing the Pension

Insurance Corporation plc (“the Company” or “the insurer”)

and Pension Insurance Corporation Group Limited (“the

Group”) Solvency and Financial Condition Report (“SFCR”) in

all material respects in accordance with the PRA Rules and

the Solvency II Regulations.

We are satisfied that:

a) throughout the financial year in question, the insurer and

Group has complied in all material respects with the

requirements of the PRA Rules and the Solvency II

Regulations as applicable at the level of the insurer and

Group; and

b) it is reasonable to believe that the insurer and Group has

continued so to comply subsequently and will continue so

to comply in future.

Signed on behalf of the Board of Directors

7

April 2022

Report of the Independent External Auditor

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202102

Opinion

Except as stated below, we have audited the following

documents prepared by the Group and the Company as at

31 December 2021:

•

The ‘Valuation for solvency purposes’ and ‘Capital

Management’ sections of the Solvency and Financial

Condition Report of the Group and the Company as at

31 December 2021, (‘the Narrative Disclosures subject to

audit’); and

•

Group templates S02.01.02, S22.01.22, S23.01.22, S32.01.22

and Company templates S02.01.02, S12.01.02, S22.01.21,

S23.01.01, S28.01.01 (‘the Templates subject to audit’).

The Narrative Disclosures subject to audit and the Templates

subject to audit are collectively referred to as the ‘Relevant

Elements of the Group Solvency and Financial Condition

Report’.

We are not required to audit, nor have we audited, and as a

consequence do not express an opinion on the Other

Information which comprises:

•

Information contained within the Relevant Elements of the

Group Solvency and Financial Condition Report set out

about above which are, or derive from the Solvency

Capital Requirement, as identified in the Appendix to this

report;

•

The ‘Business and performance’, ‘System of governance’

and ‘Risk profile’ sections of the Group Solvency and

Financial Condition Report;

•

Group templates S05.01.02, S05.02.01, S.25.02.22,

S.25.03.22;

•

Company templates S05.01.02, S05.02.01, S19.01.21,

S.25.02.21, S.25.03.21;

•

Information calculated in accordance with the previous

regime used in the calculation of the transitional measure

on technical provisions, and as a consequence all

information relating to the transitional measures on

technical provisions as set out in the Appendix to this

report;

•

The written acknowledgement by the Directors of their

responsibilities, including for the preparation of the Group

Solvency and Financial Condition Report (‘the

Responsibility Statement’);

•

Information which pertains to an undertaking that is not a

Solvency II undertaking and has been prepared in

accordance with PRA rules other than those implementing

the Solvency II Directive or in accordance with an EU

instrument other than the Solvency II regulations. ‘the

sectoral information’.

To the extent the information subject to audit in the Relevant

Elements of the Group Solvency and Financial Condition

Report includes amounts that are totals, sub-totals or

calculations derived from the Other Information, we have

relied without verification on the Other Information.

In our opinion, the information subject to audit in the

Relevant Elements of the Group Solvency and Financial

Condition Report of both Pension Insurance Corporation

Group Limited and Pension Insurance Corporation plc as at

31 December 2021 is prepared, in all material respects, in

accordance with the financial reporting provisions of the

PRA Rules and Solvency II regulations on which they are

based, as modified by relevant supervisory modifications,

and as supplemented by supervisory approvals and

determinations.

Basis for opinion

We conducted our audit in accordance with International

Standards on Auditing (UK) (ISAs (UK)) including ISA (UK) 800

and ISA (UK) 805, and applicable law. Our responsibilities

under those standards are further described in the Auditor’s

Responsibilities for the Audit of the Relevant Elements of the

Group Solvency and Financial Condition Report section of

our report. We are independent of the Group and the

Company in accordance with the ethical requirements that

are relevant to our audit of the Group Solvency and Financial

Condition Report in the UK, including the FRC’s Ethical

Standard as applied to public interest entities, and we have

fulfilled our other ethical responsibilities in accordance with

these requirements. We believe that the audit evidence we

have obtained is sufficient and appropriate to provide a

basis for our opinion.

Emphasis of Matter – special purpose basis

ofaccounting

We draw attention to the ‘Valuation for solvency purposes’

and ‘Capital Management’ sections of the Group Solvency

and Financial Condition Report, which describe the basis of

accounting. The Group Solvency and Financial Condition

Report is prepared in compliance with the financial reporting

provisions of the PRA Rules and Solvency II regulations, and

therefore in accordance with a special purpose financial

reporting framework. The Group Solvency and Financial

Condition Report is required to be published, and intended

users include but are not limited to the Prudential Regulation

Authority. As a result, the Group Solvency and Financial

Condition Report may not be suitable for another purpose.

Our opinion is not modified in respect of this matter.

Report of the external independent auditor to the Directors of Pension Insurance

Corporation Group Limited (‘the Group’) and Pension Insurance Corporation (‘the

Company’) pursuant to Rule 4.1 (2) of the External Audit Part of the PRA Rulebook

applicable to Solvency II firms

Report on the Audit of the Relevant Elements of the Group Solvency and Financial

Condition Report

Report of the Independent External Auditor continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202103

Going concern

The Directors have prepared the Group Solvency and

Financial Condition Report on the going concern basis as

they do not intend to liquidate the Company or the Group or

to cease their operations, and as they have concluded that

the Company’s and the Group’s financial position means

that this is realistic. They have also concluded that there are

no material uncertainties that could have cast significant

doubt over their ability to continue as a going concern for at

least a year from the date of approval of the Group Solvency

and Financial Condition Report (“the going concern period”).

We used our knowledge of the Group and Company, its

industry, and the general economic environment to identify

the inherent risks to its business model and analysed how

those risks might affect the Group’s and Company’s financial

resources or ability to continue operations over the going

concern period. The risks that we considered most likely to

adversely affect the Group’s and Company’s available

financial resources over this period were:

•

A significant deterioration in longevity experience,

potentially caused by market wide event(s);

•

A deterioration in the valuation of the Group’s and

Company’s investments arising from fluctuation or

negative trend in the economic environment;

•

The impact on regulatory capital solvency margins and

liquidity of movements in foreign exchange or interest

rates.

We also considered less predictable but realistic second

order impacts such as failure of counterparties / reinsurers

who have transactions with the Group / Company that

could negatively impact on the financial position.

We considered whether these risks could plausibly affect the

liquidity or Solvency in the going concern period by assessing

the Directors’ sensitivities over the level of available financial

resources indicated by the Group’s and Company’s financial

forecasts taking account of severe, but plausible adverse

effects that could arise from these risks individually and

collectively.

Our conclusions based on this work:

•

We consider that the directors’ use of the going concern

basis of accounting in the preparation of the Solvency and

Financial Condition Report is appropriate; and

•

We have not identified, and concur with the directors’

assessment that there is not, a material uncertainty

related to events or conditions that, individually or

collectively, may cast significant doubt on the company’s

ability to continue as a going concern for the going

concern period.

However, as we cannot predict all future events or conditions

and as subsequent events may result in outcomes that are

inconsistent with judgements that were reasonable at the

time they were made, the above conclusions are not a

guarantee that the Company or Group will continue in

operation.

Fraud and breaches of laws and regulations –

ability to detect

To identify risks of material misstatement due to fraud

(“fraud risks”) we assessed events or conditions that could

indicate an incentive or pressure to commit fraud or provide

an opportunity to commit fraud.

Our risk assessment procedures included:

•

Enquiring of directors, as to the companies’ high-level

policies and procedures to prevent and detect fraud, as

well as whether they have knowledge of any actual,

suspected or alleged fraud.

•

Reading Board and Audit Committee minutes.

•

Considering remuneration incentive schemes and

performance targets for management/directors.

We communicated identified fraud risks throughout the

audit team and remained alert to any indications of fraud

throughout the audit.

As required by auditing standards, and taking into account

possible pressures to meet solvency targets, we perform

procedures to address the risk of management override of

controls, in particular the risk that management may be in a

position to make inappropriate accounting entries and the

risk of bias in accounting estimates and judgements.

Accordingly, we identified a fraud risk related to accounting

estimates and judgements related to best estimate liabilities

(BEL) in the valuation of technical provisions given the

opportunity for management to manipulate assumptions

due to the subjectivity involved and given the long-term

nature of these assumptions which are more difficult to

corroborate.

On this audit we do not believe there is a fraud risk related to

revenue recognition because there is no management

judgment or estimation involved in recording the revenue

streams and the amounts are contractually derived.

In order to address the risk of fraud specifically as it relates

to the technical provisions within the Group Solvency and

Financial Condition Reporting, we involved actuarial

specialists to assist in our challenge of management. We

challenged management in relation to the appropriateness

of technical provisions and the appropriateness of the

rationale for any changes, the consistency of the selected

assumptions across different aspects of the financial

reporting process and in comparison to our understanding of

various business areas.

To address the pervasive risk as it relates to management

override, we performed procedures including:

•

Identifying journal entries and other adjustments to test

based on risk criteria and comparing the identified entries

to supporting documentation. These included those

posted by senior management, those including specific

words based on our risk criteria, those journals which were

unbalanced, those posted to unusual accounts, those

posted at the end of the period and/or post-closing entries

with little or no description and unusual journal entries

posted to either cash or borrowings.

•

Evaluating the business purpose of non-recurring transactions.

•

Assessing significant accounting estimates for bias.

No other matters related to actual or suspected fraud, for

which disclosure is not necessary, were identified.

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202104

Identifying and responding to risks of material misstatement

due to non-compliance with laws and regulations

We identified areas of laws and regulations that could

reasonably be expected to have a material effect on the

Group Solvency and Financial Condition Report from our

general commercial and sector experience ,and through

discussion with management, and from inspection of the

Group’s and Company’s regulatory and legal

correspondence, and discussed with management the

policies and procedures regarding compliance with laws and

regulations.

We communicated identified laws and regulations

throughout our team and remained alert to any indications

of non-compliance throughout the audit.

The potential effect of these laws and regulations on the

Group Solvency and Financial Condition Report varies

considerably.

Firstly, the Group and Company are subject to laws and

regulations that directly affect the Group Solvency and

Financial Condition Report including financial reporting

legislation (including related companies legislation),

distributable profits legislation, and taxation legislation and

we assessed the extent of compliance with these laws and

regulations as part of our procedures on the related financial

statement items.

Secondly, the Group and Company are subject to many

other laws and regulations where the consequences of

non-compliance could have a material effect on amounts or

disclosures in the Group Solvency and Financial Condition

Report, for instance through the imposition of fines or

litigation. We identified the following areas as those most

likely to have such as effect: liquidity and certain aspects of

company legislation recognizing the financial nature of the

Group’s and Company’s activities and its legal form. Auditing

standards limit the required audit procedures to identify

non-compliance with these laws and regulations to enquiry

of the directors and inspection of regulatory and legal

correspondence, if any. Therefore, if a breach of operation

regulations is not disclosed to us or evident from relevant

correspondence, an audit will not detect a breach.

No other matters related to actual or suspected to breaches

of laws or regulations, for which disclosure is not necessary,

were identified.

Context of the ability of the audit to detect fraud or breaches

of law or regulation

Owing to the inherent limitations of an audit, there is an

unavoidable risk that we may not have detected some

material misstatements in the financial statements, even

though we have properly planned and performed our audit

in accordance with auditing standards. For example, the

further removed non-compliance with laws and regulations

is from the events and transactions reflected in the financial

statements, the less likely the inherently limited procedures

required by auditing standards would identify it.

In addition, as with any audit, there remained a higher risk of

non-detection of fraud, as these may involve collusion,

forgery, intentional omissions, misrepresentations, or the

override of internal controls. Our audit procedures are

designed to detect material misstatement. We are not

responsible for preventing non-compliance or fraud and

cannot be expected to detect non-compliance with all laws

and regulations.

Other Information

The Directors are responsible for the Other Information.

Our opinion on the Relevant Elements of the Group Solvency

and Financial Condition Report does not cover the Other

Information and, accordingly, we do not express an audit

opinion or any form of assurance conclusion thereon.

In connection with our audit of the Group Solvency and

Financial Condition Report, our responsibility is to read the

Other Information and, in doing so, consider whether the

Other Information is materially inconsistent with the Relevant

Elements of the Group Solvency and Financial Condition

Report, or our knowledge obtained in the audit, or otherwise

appears to be materially misstated. If we identify such

material inconsistencies or apparent material

misstatements, we are required to determine whether there

is a material misstatement in the Relevant Elements of the

Group Solvency and Financial Condition Report or a material

misstatement of the Other Information. If, based on the work

we have performed, we conclude that there is a material

misstatement of this other information, we are required to

report that fact. We have nothing to report in this regard.

Responsibilities of Directors for the Group

Solvency and Financial Condition Report

The Directors are responsible for the preparation of the

Group Solvency and Financial Condition Report in

accordance with the financial reporting provisions of the

PRA rules and Solvency II regulations which have been

modified by the modifications, and supplemented by the

approvals and determinations made by the PRA under

section 138A of FSMA, the PRA Rules and Solvency II

regulations on which they are based.

The Directors are also responsible for such internal control as

they determine is necessary to enable the preparation of a

Group Solvency and Financial Condition Report that is free

from material misstatement, whether due to fraud or error;

assessing the company’s ability to continue as a going

concern, disclosing, as applicable, matters related to going

concern; and using the going concern basis of accounting

unless they either intend to liquidate the company or to cease

operations, or have no realistic alternative but to do so.

Auditor’s Responsibilities for the Audit of the

Relevant Elements of the Group Solvency and

Financial Condition Report

It is our responsibility to form an independent opinion as to

whether the Relevant Elements of the Group Solvency and

Financial Condition Report are prepared, in all material

respects, with financial reporting provisions of the PRA Rules

and Solvency II regulations on which it they based, as

modified by relevant supervisory modifications, and as

supplemented by supervisory approvals and determinations.

Our objectives are to obtain reasonable assurance about

whether the Relevant Elements of the Group Solvency and

Financial Condition Report are free from material

misstatement, whether due to fraud or error, and to issue an

auditor’s report that includes our opinion. Reasonable

assurance is a high level of assurance, but it is not a

guarantee that an audit conducted in accordance with ISAs

(UK) will always detect a material misstatement when it

exists. Misstatements can arise from fraud or error and are

considered material if, individually or in the aggregate, they

could reasonably be expected to influence the decision

making or the judgement of the users taken on the basis of

the Relevant Elements of the Group Solvency and Financial

Condition Report.

Report of the Independent External Auditor continued

A fuller description of our responsibilities is located

ontheFinancial Reporting Council’s website at:

www.frc.org.uk/auditorsresponsibilities

Other Matter

The Company has authority to calculate its Group Solvency

Capital Requirement using an internal model (“the Model”)

approved by the Prudential Regulation Authority in

accordance with the Solvency II Regulations. In forming our

opinion (and in accordance with PRA Rules), we are not

required to audit the inputs to, design of, operating

effectiveness of and outputs from the Model, or whether

the Model is being applied in accordance with the

Company’s application or approval order.

Report on Other Legal and Regulatory

Requirements

Sectoral Information

In our opinion, in accordance with Rule 4.2 of the External

Audit Part of the PRA Rulebook for Solvency II firms, the

sectoral information has been properly compiled in

accordance with the PRA rules and EU instruments relating

to that undertaking from information provided by members

of the group and the relevant insurance group undertaking.

Other Information

In accordance with Rule 4.1 (3) of the External Audit Part of

the PRA Rulebook for Solvency II firms we are also required to

consider whether the Other Information is materially

inconsistent with our knowledge obtained in the audit of

Pension Insurance Group Limited and Pension Insurance

Corporation Plc’s statutory financial statements. If, based on

the work we have performed, we conclude that there is a

material misstatement of this other information, we are

required to report that fact. We have nothing to report in this

regard.

The purpose of our audit work and to whom we

owe our responsibilities

This report of the external auditor is made solely to the

company’s directors, as its governing body, in accordance

with the requirement in Rule 4.1 (2) of the External Audit Part

of the PRA Rulebook for Solvency II firms and the terms of our

engagement. We acknowledge that the directors are

required to submit the report to the PRA, to enable the PRA

to verify that an auditor’s report has been commissioned by

the Company’s directors and issued in accordance with the

requirement set out in Rule 4.1 (2) of the External Audit Part of

the PRA Rulebook for Solvency II firms and to facilitate the

discharge by the PRA of its regulatory functions in respect of

the company, conferred on the PRA by or under the Financial

Services and Markets Act 2000.

Our audit has been undertaken so that we might state to the

Company’s directors those matters we are required to state

to them in an auditor’s report issued pursuant to Rule 4.1 (2)

and for no other purpose. To the fullest extent permitted by

law, we do not accept or assume responsibility to anyone

other than the company through its governing body, for our

audit, for this report, or for the opinions we have formed.

Philip Smart for and on behalf of KPMG LLP

15 Canada Square

London

E14 5GL

7 April 2022

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202105

Report of the Independent External Auditor continued

Report of the Independent External Auditor continued

Appendix – relevant elements of the Group Solvency and

Financial Condition Report that are not subject to audit

Group internal model

The relevant elements of the Group Solvency and Financial

Condition Report that are not subject to audit comprise:

•

The following elements of Group template S.02.01.02:

•

Row R0550: Technical provisions – non-life (excluding

health) – risk margin

•

Row R0590: Technical provisions – health (similar to

non-life) – risk margin

•

Row R0640: Technical provisions – health (similar to life)

– risk margin

•

Row R0680: Technical provisions – life (excluding health

and index-linked and unit-linked) – risk margin

•

Row R0720: Technical provisions – Index-linked and

unit-linked – risk margin

•

The following elements of Group template S.22.01.22

•

Column C0030 – Impact of transitional measures on

technical provisions

•

Row R0010 – Technical provisions

•

Row R0090 – Solvency Capital Requirement

•

The following elements of Group template S.23.01.22

•

Row R0020: Non-available called but not paid in

ordinary share capital at group level

•

Row R0060: Non-available subordinated mutual

member accounts at group level

•

Row R0080: Non-available surplus at group level

•

Row R0100: Non-available preference shares at

grouplevel

•

Row R0120: Non-available share premium account

related to preference shares at group level

•

Row R0150: Non-available subordinated liabilities

atgrouplevel

•

Row R0170: The amount equal to the value of net

deferred tax assets not available at the group level

•

Row R0190: Non-available own funds related to other

own funds items approved by supervisory authority

•

Row R0210: Non-available minority interests at

grouplevel

•

Row R0380: Non-available ancillary own funds at

grouplevel

•

Rows R0410 to R0440 – Own funds of other

financialsectors

•

Row R0680: Group SCR

•

Row R0740: Adjustment for restricted own fund items in

respect of matching adjustment portfolios and ring

fenced funds

•

Row R0750: Other non-available own funds

•

Elements of the Narrative Disclosures subject to audit

identified as ‘unaudited’

Solo internal model

The relevant elements of the Group Solvency and Financial

Condition Report that are not subject to audit comprise:

•

The following elements of template S.02.01.02:

•

Row R0550: Technical provisions - non-life (excluding

health) - risk margin

•

Row R0590: Technical provisions - health (similar to

non-life) - risk margin

•

Row R0640: Technical provisions - health (similar to life)

- risk margin

•

Row R0680: Technical provisions - life (excluding health

and index-linked and unit-linked) - risk margin

•

Row R0720: Technical provisions – Index-linked and

unit-linked – risk margin

•

The following elements of template S.12.01.02

•

Row R0100: Technical provisions calculated as a sum

ofBE and RM – Risk margin

•

Rows R0110 to R0130 – Amount of transitional measure

on technical provisions

•

The following elements of template S.17.01.02

•

Row R0280: Technical provisions calculated as a sum

ofBE and RM – Risk margin

•

Rows R0290 to R0310 – Amount of transitional measure

on technical provisions

•

The following elements of template S.22.01.21

•

Column C0030 – Impact of transitional measures

ontechnical provisions

•

Row R0010 – Technical provisions

•

Row R0090 – Solvency Capital Requirement

•

The following elements of template S.23.01.01

•

Row R0580: SCR

•

Row R0740: Adjustment for restricted own fund items

inrespect of matching adjustment portfolios and ring

fenced funds

•

The following elements of template S.28.01.01

•

Row R0310: SCR

•

Elements of the Narrative Disclosures subject to audit

identified as ‘unaudited

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202106

The Solvency and Financial Condition Report (“SFCR”) is an annual report that is required to be produced under UK law, as

part of the Solvency II regime. References to the Solvency II Directive should be taken as referring to the transposition of that

Directive into UK legislation which have been retained for convenience and comparability with instances of the SFCR from

prior years.

The Group has permission to produce a single SFCR, covering both Pension Insurance Corporation plc (“PIC”, or “the

Company”) and Pension Insurance Corporation Group Limited (“PICG”, or “the Group”). This requirement is set out in a

direction made by the Prudential Regulatory Authority (“PRA”) on 6 November 2019. This direction is in force until 30 June 2022.

The SFCR is a public document and is published on the Company’s website. It is also provided to the Company’s prudential

regulator, the PRA.

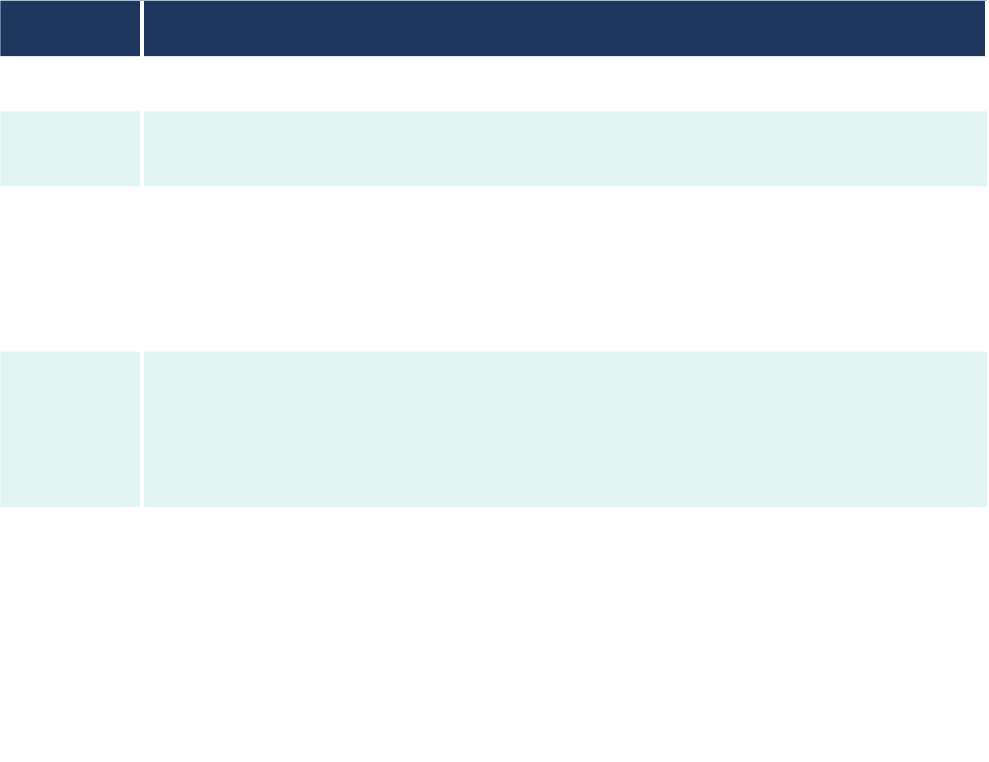

The content of the SFCR is prescribed by PRA regulation, and must contain the following sections:

SECTION DESCRIPTION OF CONTENT

Business and Performance Provides the basic information on the Group and Company,

and gives a summary of the business performance during

the year in question.

System of Governance Provides governance information on the Group and

Company including Board and Committee structure,

responsibilities, and details of the principal process.

Risk Profile Provides qualitative and quantitative information regarding

the risks that face the Group and Company, and how they

are managed.

Valuation for Solvency Purposes Provides values for the Group and Company’s assets and

liabilities in accordance with International Financial

Reporting Standards (“IFRS”) and Solvency II rules, gives

details on the assumptions used in the valuations, and

provides explanations on valuation differences between

IFRS and Solvency II.

Capital Management Provides detail on the regulatory capital (own funds) which

the Group and Company must hold in line with Solvency II

rules, and the composition of such own funds.

PIC is authorised to write long-term insurance business by the PRA and regulated by the PRA and the Financial Conduct

Authority (the “FCA”).

Pension risk transfer products are used by pension funds to transfer to an insurance company the risks and liabilities arising

from the benefit promises made to pension fund members. Insurance is also used as a means by which the ultimate

responsibility to pay the benefit promises is transferred to the insurance company through the issuance of an individual

annuity insurance policy to the pension fund member.

The Company takes a leading role in developing and informing the pensions market through pension trustee training events.

PIC publishes regular papers on the pensions market and information on how to address certain key issues for the

commercial and the public sector, such as managing pension costs and risk inherent in pension schemes. It has an active

thought leadership programme in dealing with government, corporate sponsors and pension trustees and working with them

on pension solutions in the public and private sectors.

The Company originates new business through active engagement with, and marketing to, pension fund trustees and their

advisors, as well as to corporate sponsors of such funds.

PIC is the primary operating subsidiary of the Group.

A summary of the content of each SFCR section is provided below:

Business and performance

The Group and Company continued to trade profitably during 2021 despite turbulent market conditions and the uncertainty

caused mainly by the ongoing Covid-19 pandemic. The Group has shown resilience and remains financially strong and

profitable with a Solvency II ratio of 169% in PICG and 168% in PIC (2020: 158% in PICG and 157% PIC). The Group profit before

tax was £393 million for the year (2020: £276 million) and PIC’s profit before tax was £394 million (2020: £276 million).

Summary (unaudited)

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202107

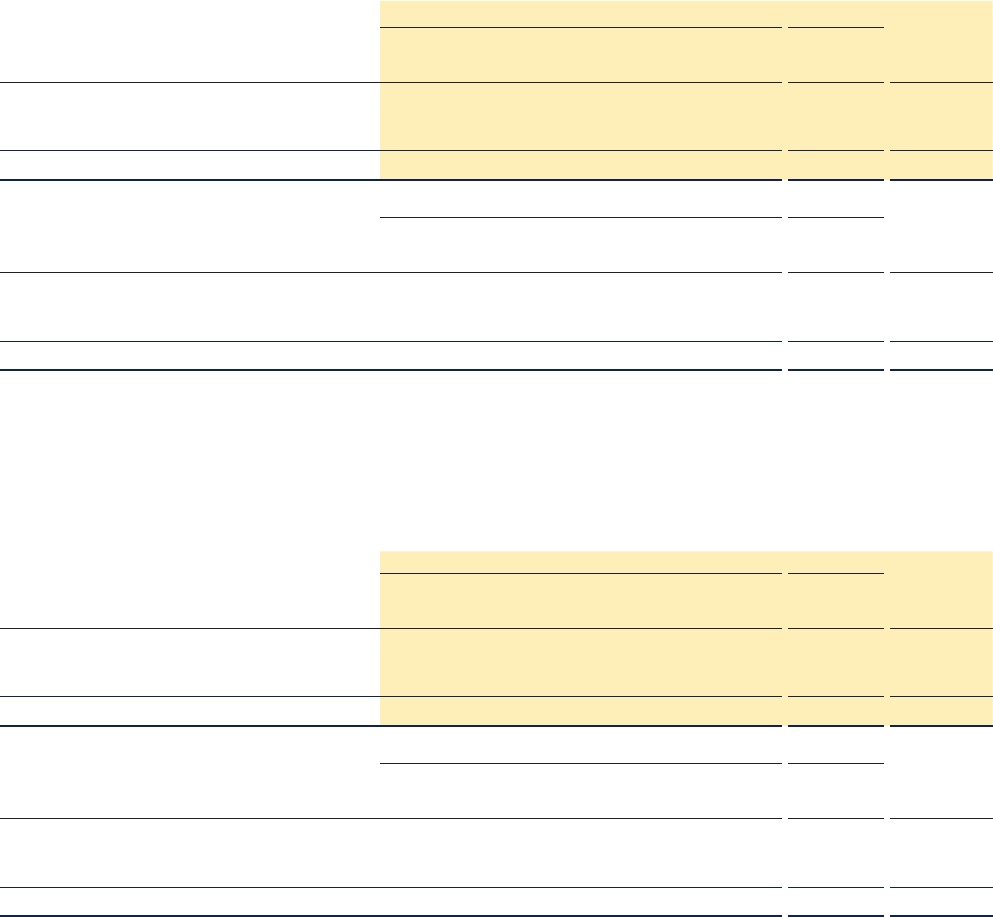

Statement of comprehensive income highlights – PICG

2021

£m

2020

£m

Gross premiums written 4,702 5,649

Net premium revenue earned 3,856 5,132

Investment return (including commissions earned) 210 4,091

Total revenue 4,066 9,223

Net claims paid (1,785) (1,683)

Change in net insurance liabilities (1,601) (6,997)

Operating expenses (198) (194)

Finance costs (89) (73)

Total claims and expenses (3,673) (8,947)

Profit before tax 393 276

Statement of comprehensive income highlights – PIC

2021

£m

2020

£m

Gross premiums written 4,702 5,649

Net premium revenue earned 3,856 5,132

Investment return (including commissions earned) 210 4,091

Total revenue 4,066 9,223

Net claims paid (1,785) (1,683)

Change in net insurance liabilities (1,601) (6,997)

Operating expenses (198) (195)

Finance costs (88) (72)

Total claims and expenses (3,672) (8,947)

Profit before tax 394 276

Premiums

A combination of lower market activity in the first half of the year and our adherence to our policy of only writing business

which meets long-term value targets, led to a reduction in gross premiums written to £4,702 million from £5,649 million in 2020.

The Group completed fourteen new business transactions during the year (2020: seven), including the largest single

transaction ofthe year, the £2.2 billion Metal Box buyout. We continue to be selective in underwriting those risks where we

expect to generate an adequate return within our risk appetite.

Net premiums earned represent the gross premiums written less premiums ceded to reinsurers. Premiums ceded to

reinsurersincreased due to the completion of asset backed reinsurance transactions covering approximately £750 million

(2020: £385 million) of liabilities. In total, seven (2020: eight) new reinsurance contracts were concluded in 2021.

Investment return

Investment return comprises income received on fixed income securities, derivatives and investment property, and

unrealised and realised gains and losses on these investments.

Interest income on fixed securities increased to £1,054 million in 2021 from £1,027 million in 2020, reflecting the growth in the

investment portfolio during the year.

The net movement in the fair value of assets, including realised and unrealised items, was a loss of £1,029 million compared

with a gain of £3,110 million in 2020. This comprises realised gains of £307 million (2020: £634 million) and unrealised losses of

£1,336 million (2020: gain of £2,476 million).

The unrealised losses recognised in 2021 are primarily due to higher risk-free rates.

Other investment return and commissions amounted to £185 million (2020: loss of £46 million) primarily representing gains on

derivative contracts.

It is important to note that fair value gains and losses included in investment return in the income statement are largely offset

by changes in insurance liabilities, also in the income statement. Therefore, there is minimal impact on profit before tax.

Claims paid

Net claims paid comprises of gross claims paid, which are pension payments to our policyholders, less any payments

received from reinsurers. Net claims paid increased from £1,683 million in 2020 to £1,785 million in 2021, reflecting the

increasednumber of customers.

Summary (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202108

Change in net insurance liabilities

Change in net insurance liabilities represents the change in the gross insurance liabilities less the movement in

reinsuranceassets.

The change in net insurance liabilities mainly reflects the increase in the number of policies by 17,200 to 289,600 partially

offset by market movements, principally the increase in risk-free rates seen in the year, and the impact of assumption

changes.

Operating expenses

The operating expenses of both PIC and PICG were £198 million in 2021 (2020: PIC £195 million, PICG £194 million). This includes

project spend of £38 million (2020: £45 million) primarily to support the forthcoming introduction of the new IFRS 17 accounting

standard, as well as spend on new asset and capital models. Excluding these project costs, the remaining increase in spend

mainly reflects an increase in equity release mortgage origination fees.

Finance costs

Finance costs represent the interest payable on borrowings and finance lease costs. The expense in PIC of £88 million in 2021

(2020: £72 million) represents the interest payable on the five (2020: five) subordinated debt securities issued. This increase

was due to the full year effect of the two Tier 2 debt issues made in 2020. The expense in PICG of £89 million (2020: £73 million)

includes an additional £1 million (2020: £1 million) in respect of finance lease costs. The Restricted Tier 1 (“RT1”) debt issued in

July 2019 has been accounted for as equity under IFRS and as such interest on these notes is not included in finance costs

and is instead recognised as dividends when paid.

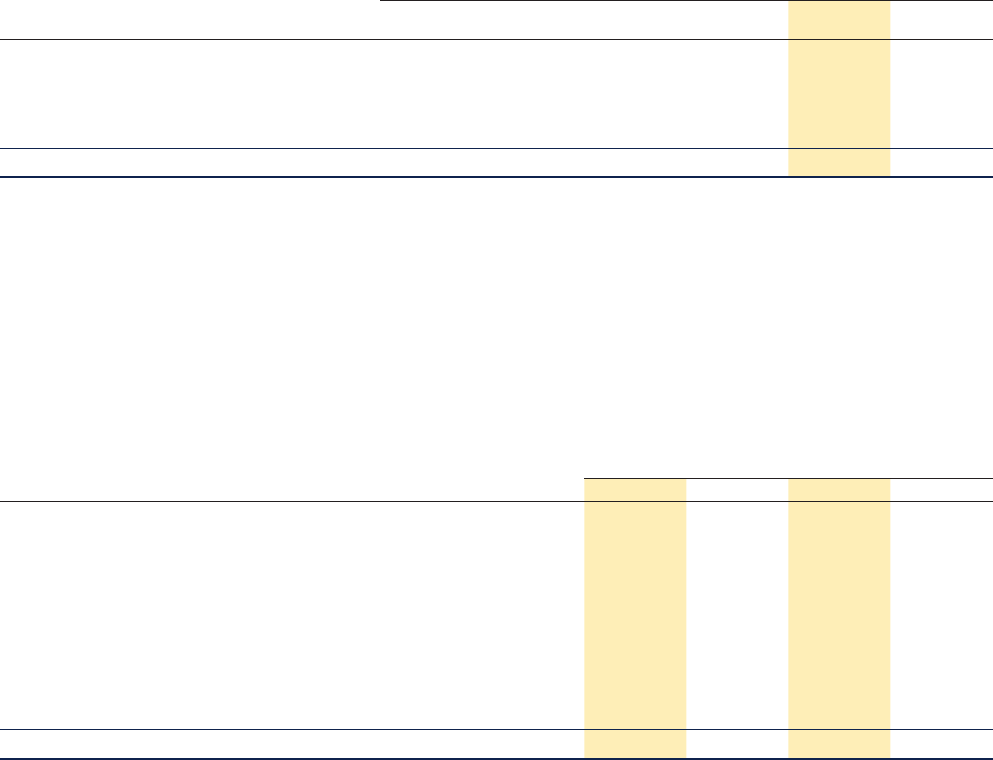

Statement of financial position review – PICG

Statement of financial position extract

2021

£m

2020

£m

Financial investments 51,143 49,648

Reinsurance assets 3,350 2,773

Derivative assets 15,018 21,936

Gross insurance liabilities (47,013) (44,835)

Derivative liabilities (16,997) (24,340)

Borrowings (1,590) (1,589)

Other net assets 554 574

Total equity 4,465 4 ,167

Statement of financial position review – PIC

Statement of financial position extract

2021

£m

2020

£m

Financial investments 51,316 49,742

Reinsurance assets 3,350 2,773

Derivative assets 15,018 21,936

Gross insurance liabilities (47,013) (44,835)

Derivative liabilities (16,997) (24,340)

Borrowings (1,590) (1,589)

Other net assets 345 456

Total equity 4,429 4,143

At the end of 2021, the Group had total financial investments of £51.1 billion (PIC: £51.3 billion), compared with £49.6 billion

(PIC:£49.7 billion) at the end of 2020. The assets in which the Group invests are carefully chosen in order to match the

policyholder obligations that they are designed to pay. The Group’s investment strategy is to select assets that generate

cash flows to match our future claims payments in both timing and amount. This means that the value of assets and

liabilities should move broadly in tandem as factors such as interest and inflation rates change.

The credit quality of our investment portfolio continues to remain strong which has ensured that the Group did not

experience any defaults in 2021 (2020: none) and that downgrades to sub-investment grade credit were less than

0.1%(2020: 0.4%) of the credit portfolio (including private investments but excluding gilts).

The increase in reinsurance assets during the year primarily reflects the asset backed reinsurance arrangements completed

during the year. In 2021, the Group reinsured longevity exposure on £4.0 billion of reserves (2020: £6.6 billion), andat

31 December 2021, 85% of the Group’s gross longevity related reserves had been reinsured (2020: 84%). The Group has14

reinsurance counterparties (2020: 14), all of which have a credit rating of A or above.

The increase in insurance liabilities in 2021 reflects the addition of new business liabilities partly offset by movements in

economic factors during the year coupled with claims paid and the impact of changes in assumptions.

Gross derivative assets and derivative liabilities have both decreased during the year, by £6.9 billion and £7.3 billion

respectively. The net increase in the year across all derivative assets and liabilities was £425 million. The Group uses

derivatives to hedge out certain market risks, in particular inflation, interest rates and currency risks associated with both

new and existing business. The decrease in the gross derivative asset and liability balances is as a result of market

Summary (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202109

movements partially offset by new business written in the year. It should be noted that all derivative contracts are fully

collateralised using a custodian, and as such present little credit risk in the event of a derivative counterpartydefault.

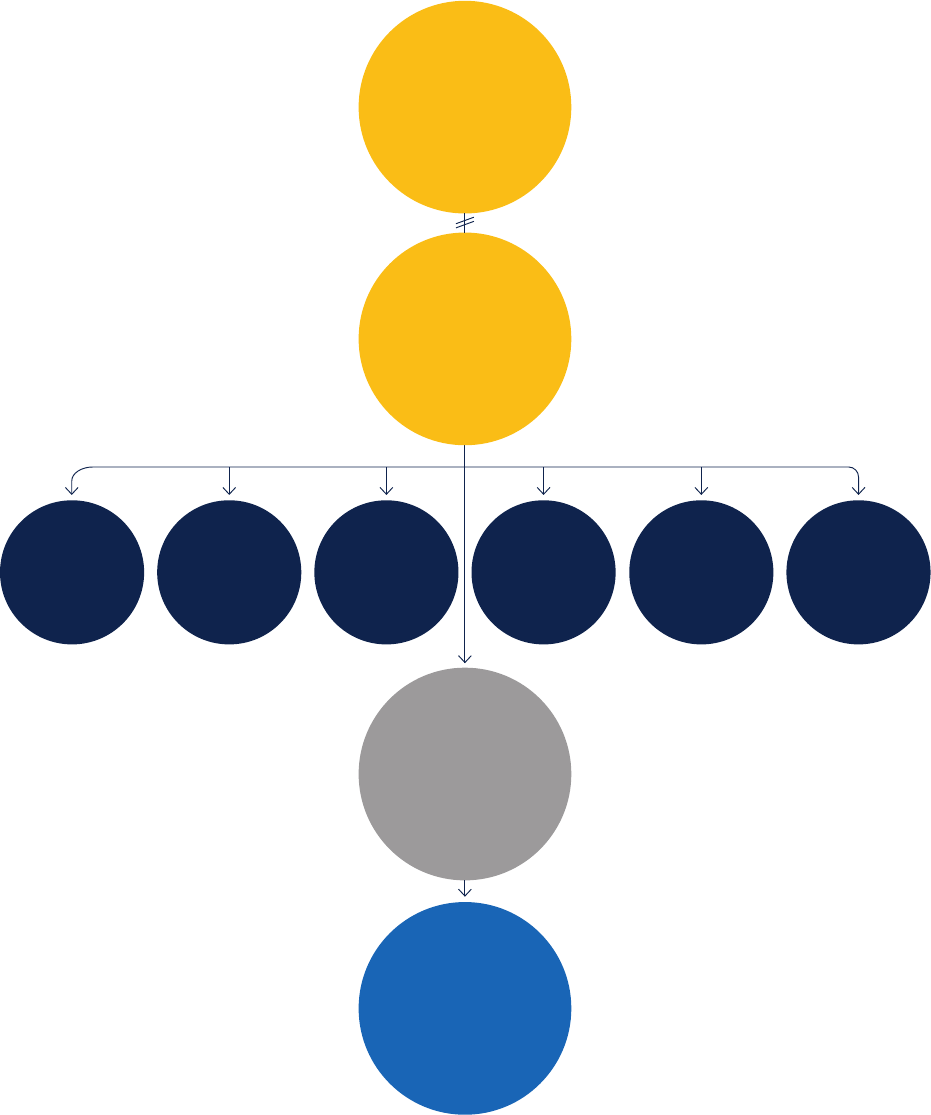

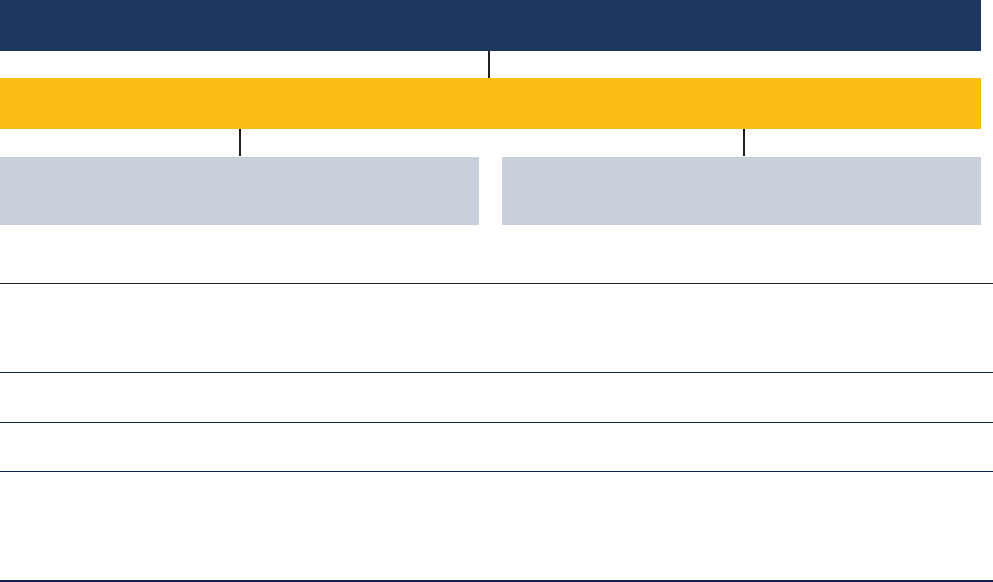

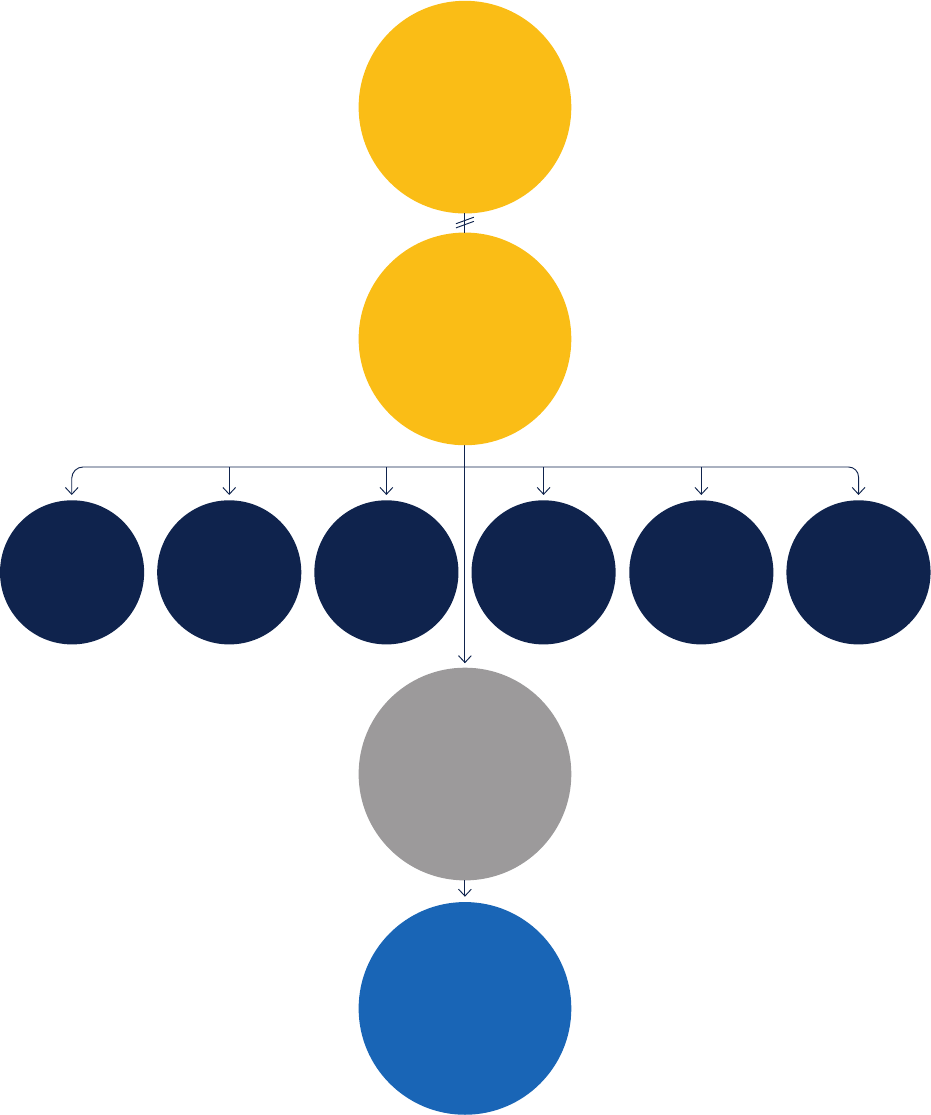

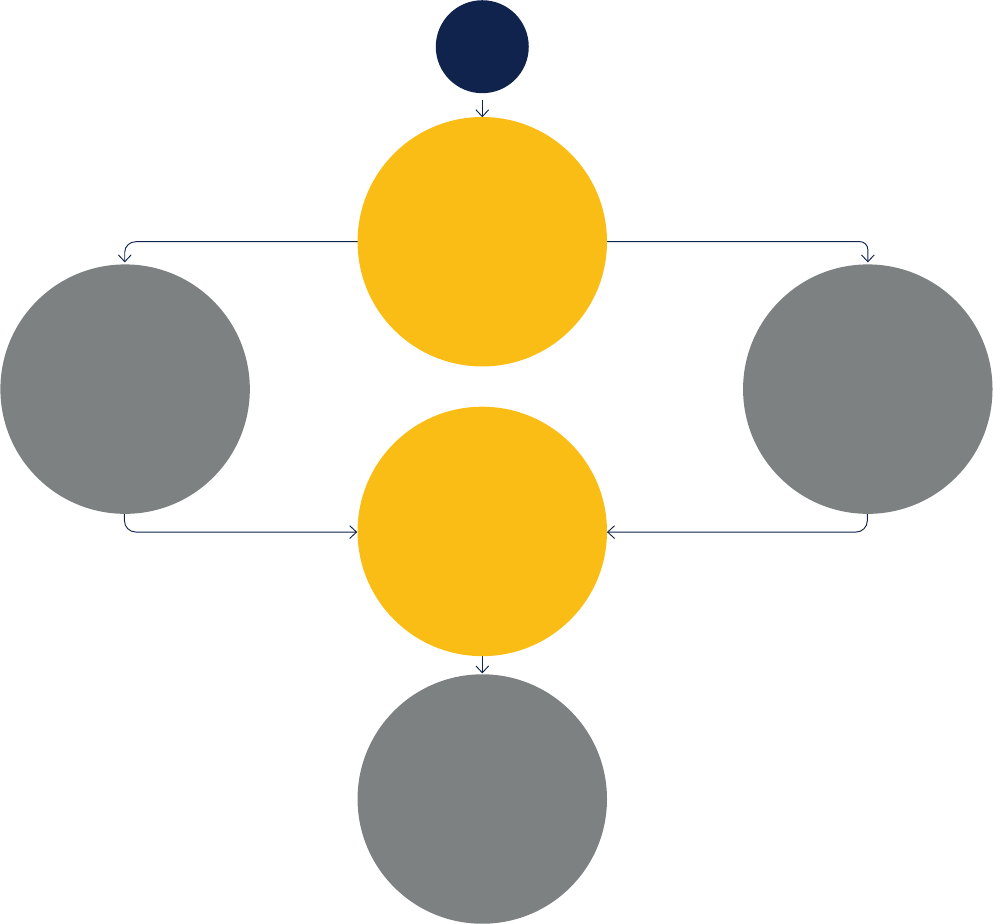

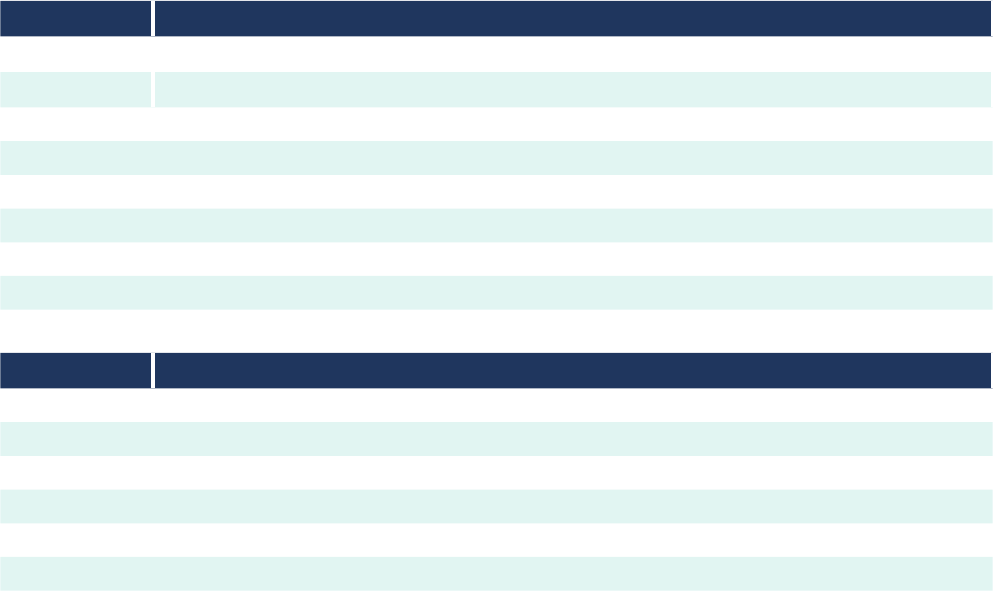

System of Governance

PIC’s governance structure is in line with the “three lines of defence” model which is operated by the Group. The Board

delegates specific responsibilities to the Board committees, which assist the Board in its oversight and control of

thebusiness.

There are currently six Board committees: Audit, Environmental, Social and Governance (“ESG”), Investment and Origination,

Nomination, Remuneration and Risk. The Investment and Origination Committee considers matters specific to PIC. The five

remaining committees consider matters specific to PIC and the Group, as per the delegations in their terms of reference

(further details are provided below). Members of the committees are appointed by the Board on recommendation of the

Nomination Committee in consultation with the committees’ chairmen.

Summary (unaudited) continued

Nomination

Committee

Audit

Committee

Risk

Committee

Investment and

Origination

Committee

Remuneration

Committee

ESG

Committee

Executive

Committee

Management

and Operating

Committees

PICG Board

PIC Board

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202110

Audit Committee

The Committee works closely with the Risk Committee and has responsibility for ensuring the company fulfills its

responsibilities regarding financial reporting, the effectiveness of internal controls, the risk management systems and

processes, compliance matters, and the internal audit function and external audit process.

ESG Committee

In December 2021 the Group established an ESG Committee which meets quarterly to consider and oversee all ESG related

matters. The purpose of the Committee is to ensure that the Board and its Committees provide oversight of the Group’s ESG

strategy and activities, and that the Group complies with legal and regulatory requirements in respect of ESG, enabling the

Group to make the right decisions for the long-term benefits of our policyholders.

Investment and Origination Committee

The Committee oversees the investment policy and investment strategy for PIC, ensuring that ESG is integrated into decision

making and provides oversight of the operation of PIC’s investment portfolios. It also oversees PIC’s new business and

reinsurance origination.

Nomination Committee

The Committee is responsible for reviewing the structure, size and composition of the Board and its committees and for

recommending changes to the Board and setting succession plans for executive and non-executive directors and senior

management within the Group.

Remuneration Committee

The Committee oversees the establishment and implementation of a remuneration policy for employees and directors,

designed to support the long-term business strategy and values of the Group as a whole, as well as promoting effective risk

management and complying with applicable legal and regulatory requirements.

Risk Committee

The Committee provides oversight and advice to the Board on the current and future risk exposure of the Group including

oversight of the future risk strategy; determination of risk appetite and tolerance; and internal controls required to manage

risk and the effectiveness of the risk management framework, in conjunction with the Audit Committee.

Risk Profile

The Group and Company quantify their exposure to different types of risk using their Internal Model, which was approved for

use by the PRA in December 2015. Major Model Changes were approved by the PRA in December 2017 relating to longevity

and inflation and in December 2020 relating to Equity Release Mortgages.

The Group’s total Solvency Capital Requirement (“SCR”) represents the amount of capital the firm must hold to protect it

from extreme risk events and comply with regulatory requirements. The component risks which make up the SCR are

detailed in Section C.

The Group’s risk profile has remained stable over the reporting period.

Valuation for Solvency Purposes

The table below summarises the Group and Company’s assets and liabilities valued in accordance with its statutory

accounting basis (IFRS), and the Solvency II regulatory basis at 31 December:

2021

Group Company

Solvency

£m

IFRS

£m

Solvency

£m

IFRS

£m

Total Assets 69,676 70,293 69,626 70,242

Total Liabilities 64,555 65,828 64,555 65,813

Excess of Assets over Liabilities/Equity 5,121 4,465 5,071 4,429

2020

Group Company

Solvency

£m

IFRS

£m

Solvency

£m

IFRS

£m

Total Assets 74,338 75,080 74,288 75,045

Total Liabilities 69,278 70,913 69,270 70,902

Excess of Assets over Liabilities/Equity 5,060 4,167 5,018 4,143

Differences in the valuation of assets and liabilities between the two bases are driven by the following:

•

The Solvency II Risk Margin (net of transitional measures for technical provisions (“TMTP”)) which is an addition to the

Solvency II best estimate liabilities but is not required under IFRS;

•

IFRS prudent margins in the projected liability cashflows (for example, via the expense and demographic assumptions)

which increase IFRS liabilities relative to the Solvency II best estimate liabilities;

•

Differences in the valuation discount rate, used to discount the liability cashflows, which is prescribed for Solvency II but

determined by PIC for IFRS (and includes prudent margins);

Summary (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202111

•

Valuation of subordinated debt liabilities, which are at amortised cost for IFRS purposes and are at fair value under

Solvency II; and

•

Differences related to deferred tax assets and liabilities.

The valuation differences above are explained in greater detail in section D.

Capital Management

At 31 December 2021, PICG’s Solvency II ratio was 169% (PIC: 168%) (2020: PICG 158% and PIC: 157%) and it had surplus funds of

£2,731 million (PIC: £2,701 million) (31 December 2020: PICG: £2,465 million; PIC: £2,449 million) in excess of its SCR as calculated

by the internal model. Despite the impact of adverse market conditions and significant new business volumes written in 2021,

a combination of effective underwriting, reinsurance and capital management ensured that the Solvency II ratio remained

robust.

The table below summarises the Group and Company’s capital and solvency position as at 31 December:

2021 Group Company

Own Funds (£m) 6,699 6,669

SCR (£m) 3,968 3,968

Solvency II surplus (£m) 2,731 2,701

Solvency II ratio % 169% 168%

2020 Group Company

Own Funds (£m) 6,726 6,710

SCR (£m) 4,261 4,261

Solvency II surplus (£m) 2,465 2,449

Solvency II ratio % 158% 157%

Summary (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202112

A.1 Business

The full legal name of the undertaking is Pension Insurance Corporation plc. It is a Public Limited Company, registered in

England and Wales with the company registration number 05706720.

PIC is authorised by the Prudential Regulation Authority, 20 Moorgate, London EC2R 6DA and regulated by the Financial

Conduct Authority, 12 Endeavour Square, London, E20 1JN and the Prudential Regulation Authority (FRN 454345).

The principal activity of PIC is the provision of pension risk transfer contracts to corporate pension schemes (also known as

“pension insurance” or “bulk annuities”). Pension risk transfer products are used by pension funds to transfer to an insurance

company the risks and liabilities arising from the benefit promises made to pension fund members. Insurance is also used as

a means by which the ultimate responsibility to pay the benefits promised is transferred to the insurance company through

the issuance of an individual annuity insurance policy to the pension fund member.

A simplified group structure chart, and a description of the Group as at 31 December 2021 is set out below:

PENSION INSURANCE CORPORATION GROUP LIMITED (“PICG”)

PIC HOLDINGS LIMITED (“PICH”)

PENSION SERVICES CORPORATION LIMITED (“PSC”)PENSION INSURANCE CORPORATION PLC (“PIC”)

Group Undertakings

Country of

Incorporation

Principal

Activity

Pension Insurance Corporation

GroupLimited

England Holding company for the other companies within the Group,

owning 100% of the equity. It has no employees, and incurs

minimal administrative expenses. It also operates share

incentive plans for the benefit of the employees of the Group.

PIC Holdings Limited England An intermediate holding company, and has no material assets

or liabilities in the context of the Group.

Pension Insurance Corporation plc England Provision of insurance annuity products to corporate

pensionschemes and their members.

Pension Services Corporation Limited England Service company of the Group, and employs all the staff which

are responsible for the performance of the Group’s activities. It

also enters into the majority of material contracts (with the

exception of pension insurance contracts) on behalf of the

Group.

The Group and Company prepare their financial statements in accordance with IFRS and those parts of the Companies Act

2006 applicable to companies reporting under IFRS. There are no differences between the scope of the Group for the

consolidated financial statements and the scope under the default accounting consolidation method for Solvency purposes.

The External Auditor to the Group is KPMG LLP, 15 Canada Square, London E14 5GL.

As presented in the Summary, the Group made an IFRS profit before tax of £393 million in 2021 (2020: £276 million), and the

Company made an IFRS profit before tax of £394 million in 2021 (2020: £276 million).

The tables in sections A.2 to A.4 below present extracts from the Group’s and Company’s IFRS Statements of Comprehensive

Income, splitting the IFRS income and expense items between underwriting activity (section A.2), investment activity

(sectionA.3) and other activity (section A.4). Comparative information has been presented where available.

A. Business and Performance (unaudited)

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202113

A.2 Performance of underwriting activity

In addition to the statutory results presentation as outlined above, the Group also chooses to analyse its IFRS results on an

alternative performance metric, ‘adjusted operating profit before tax’, which is a non-GAAP measure of long-term value

creation, a key outcome of the Group’s business model. It reflects the Group’s activities which are core to our business and

the management choices and decisions around those activities. These activities include the writing and management

ofpension insurance contracts (buyouts and buy-ins), the management of risk through reinsurance, and the day-to-day

investment and management of the insurance assets and liabilities. In essence, it gives stakeholders a more accurate view

ofthe expected long-term investment returns on the assets backing policyholder and shareholder funds, with an allowance

for the corresponding expected movements in liabilities. This basis reflects the long-term trading activities of the Group

better than the IFRS reported profit before taxation.

Information on premiums, claims and changes in technical provisions, which can be considered as key elements of

underwriting performance, is presented by Solvency II line of business in Quantitative Reporting Template (“QRT”) S.05.01.02

inAppendix B of this report.

Adjusted operating profit

2021 2020 (restated)

PICG

£m

PIC

£m

PICG

£m

PIC

£m

Expected return from operations 288 288 274 274

New business and reinsurance profit 167 167 187 187

Underlying profit 455 455 461 461

Change in valuation assumptions 315 315 292 292

Experience and other variances (77) (77) (253) (253)

Finance and project costs (160) (159) (151) (151)

Adjusted operating profit before tax 533 534 349 349

Investment related variances (173) (173) (106) (106)

Add back: RT1 coupon (treated as a dividend for statutory purposes) 33 33 33 33

Profit before taxation 393 394 276 276

During 2021, the definition of adjusted operating profit before tax was amended to take account of three refinements

tothemethodology:

1. New business profit has been redefined to align the reported new business profitability with the assumptions used in

thepricing of new business. Any variance between pricing and current valuation assumptions is then recognised as an

experience variance outside of underlying profit that will reverse over time. There is no change to adjusted operating

profit before tax.

2. Reinsurance profit has been restated to recognise short term timing differences, and their reversal, within experience

variances. This is consistent with underlying profit being an ‘expected’ profit measure. There is no change to adjusted

operating profit before tax.

3. The cost of the RT1 interest has been recognised within finance costs. This is to align the reporting across all bases and

reflects the way management and rating agencies view these financing costs. The treatment for the statutory IFRS

statement of comprehensive income remains unchanged, i.e. the RT1 interest is treated as a dividend, and therefore

theRT1 interest is added back before profit before tax in the alternative profit metric.

The 2020 comparatives have been restated accordingly.

The Group’s adjusted operating profit before tax was £533 million (PIC: £534 million), an increase of 53% from 2020 (PIC: 53%).

This was primarily due to management actions and assumption changes and a lower adverse experience variance. More

detail on the main components of adjusted operating profit is set out below.

Underlying profit

This item comprises the expected returns arising from the management of the Group’s assets and liabilities. This is derived

byusing assumptions about long-term returns on the underlying investment portfolio backing liabilities, and on the surplus

assets of the Group.

It also includes the impact on profit of writing new pension risk transfer contracts based on target asset mix assumptions

andthe impact of entering into new contracts of reinsurance.

Underlying profit of £455 million in 2021 was broadly in line with 2020 (2020: £461 million). Within this figure, expected return

from operations of £288 million was higher than last year (2020: £274 million) mainly reflecting a higher assumed longer-term

rate of return due to the increase in interest rates seen in the year, partially offset by lower credit spreads in 2021.

A. Business and Performance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202114

New business and reinsurance profit of £167 million was lower than 2020 (£187 million). Within this result, new business profits

were higher than last year, despite lower volumes, reflecting a favourable business mix. This was offset by a reduced benefit

from reinsurance on the in-force book.

Reinsurance transactions in 2021 covered £4.0 billion of liabilities compared to £6.6 billion of liabilities reinsured in 2020.

Changes in valuation assumptions

The Group sets assumptions in respect of the in-force liabilities and new business acquired during the year. Management

regularly review these assumptions to ensure that they reflect the characteristics of our book and wider market practice.

As part of management’s review of assumptions in 2021, the Group updated several assumptions including those in respect

of credit defaults, maintenance expenses, investment management fees, inflation and the IFRS liquidity premium rate.

Thisresulted in a profit of £315 million.

To ensure that our default and downgrade expectations are appropriate, we undertake a regular update of our long-term

expectations based on data provided by rating agencies. The update for 2021 resulted in a release of £116 million, which

reflects the lesser likelihood of downgrades in our investment portfolio, and has been impacted by various actions taken

bythe business in recent years. The credit default reserve was £2.7 billion as at 31 December 2021 (31 December

2020: £2.9 billion).

During the year, after reviewing our contractual custodian fees, the assumption for investment management fees was

updated resulting in a release of reserves of £104 million.

Following the Retail Price Index (“RPI”) reform announced by the Chancellor in November 2020 which proposes to align RPI to

the Consumer Prices Index including owner occupiers’ housing costs (“CPIH”) after 2030, we took the opportunity to update

our longer-term inflation assumptions and refine our inflation modelling to take account of both Consumer Price Index (“CPI”)

and RPI volatility. This resulted in an increase in IFRS surplus of £70 million.

In addition, there were several other assumption changes made in the year which included an update to the reinvestment/

disinvestment rate used for the IFRS liquidity premium calculation and an update to the maintenance expense assumption

incorporating the latest expense budgets and following a review and update of expense allocations. In 2020, total reserve

releases of £292 million were in respect to changes in assumptions for longevity and expenses.

Experience variances and other costs

Experience variances, which reflect the difference between the assumptions used for pricing within the new business line

and those used for reserving, actual claims experience in the period compared to the expected amounts and the impacts

ofdata updates on underlying policyholder information, gave rise to a loss of £77 million in 2021 (2020: loss of £253 million).

In 2020, the negative experience variance was primarily due to differences between the maintenance expense assumption

used in pricing compared to those used in the valuation basis. This gave rise to a negative experience variance of £158 million

which was largely offset in the year by a reserve release within changes in valuation assumptions. In addition, data updates

resulted in a loss of £46 million.

Finance and Other Costs

The interest costs of the subordinated Tier 2 debt capital issued by PIC, rose to £88 million in 2021 (PICG: £88 million) from

£73 million the previous year (PICG: £73 million). This increase was due to the full year effect of the two Tier 2 debt issues

made in 2020.

Interest coupons paid on the RT1 Debt issued by PIC were £33 million (PICG: £33 million) and were unchanged from 2020

(PICG:£33 million).

Project costs in 2021 were £38 million (PICG: £38 million) compared to 2020 costs of £45 million (PICG: £45 million).

Investment related variances

Investment related variances gave rise to a loss of £173 million in the year (2020: loss of £106 million).

As noted above, adjusted operating profit before tax is based on expected long-term investment returns which are

calculated using management assumptions of the returns on the assets backing policyholder and shareholder funds with an

allowance for the corresponding expected movements in liabilities. The long-term rates of return earned on excess assets

are derived with reference to the expected longer-term yield of the underlying assets. Profit before tax includes the actual

investment returns earned in the period on assets backing insurance liabilities and surplus assets. Actual investment returns

in the year, on a mark to market basis, will differ from the expected longer-term returns due to short-term impacts from

market movements. The difference between the actual and the expected long-term rates of return, coupled with the impact

of changes in economic assumptions on liabilities and the difference between the short-term actual asset mix and the

expected long-term asset mix on new business transactions during the year are included within investment related

variances, outside of adjusted operating profit before tax.

A. Business and Performance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202115

The Group carefully manages its exposure to market and other economic risks in order that we are able to fulfil our purpose

over the long-term. As such the Group’s hedging strategy is primarily designed to protect the solvency balance sheet. This is

achieved by entering into derivative hedging contracts in accordance with our risk framework. However, due to the differing

requirements of the Solvency II and IFRS reporting metrics, there is a mismatch between the Solvency II and the IFRS balance

sheet hedging strategies. This mismatch, and the resulting volatility, is included within the investment related variance line.

The impact of downgrades and management actions which were taken to improve the resilience of the balance sheet are

also both included here.

In 2021, the adverse investment variance of £173 million was primarily due to significant economic volatility in the year, in

particular rising GBP risk free rates and credit spread movements partially offset by higher inflation.

Other operational highlights

In total, in 2021, PIC was responsible for the current and future pension payments of 282,900 (2020: 271,500) individuals,

including those with individual policies, and those for whom the trustees of the underlying pension schemes retain ultimate

responsibility.

At 31 December 2021, 85% of PIC’s total longevity exposure on a regulatory solvency basis was reinsured to third party,

investment grade reinsurer counterparties (2020: 84%).

A.3 Performance of investment activity

The investment performance (including commissions earned), as presented in the table below, is a reflection of income, gains

(realised and unrealised), losses and expenses arising from the investment portfolio owned by the Group.

Group and Company

Investment return: by Solvency II Asset Class

2021

£m

2020

£m

Government bonds 59 1,995

Corporate bonds (188) 1,865

Collective Investment undertakings 119 44

Cash and deposits (2) 1

Collateralised securities 1 27

Mortgages and loans (220) 652

Derivative based instruments 440 (494)

Commissions earned 1 1

Investment Return 210 4,091

Investment management expenses (42) (29)

Total 168 4,062

Investment return comprises income received on fixed income securities, derivatives and investment property, and

unrealised and realised gains and losses on these investments. The above table allocates investment return across the SII

asset classes.

It is important to note that fair value gains and losses included in investment return in the income statement are largely offset

by changes in insurance liabilities, also in the income statement. Therefore, there is minimal impact on profit before tax.

A.4 Performance of other activities

Pension Insurance Corporation Group Limited

Group corporation tax charges, including those incurred by PIC, were £82 million during the year (2020: £54 million).

Pension Insurance Corporation plc

The Company incurred corporation tax charges of £81 million for the year ended 31 December 2021 (2020: £53 million).

A. Business and Performance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202116

A.5 Any other information

Economic uncertainty and market volatility

We expect the trend of uncertainty and volatility in the financial markets to continue into 2022. The clear need for the global

economies to address climate change is also driving global economic uncertainty. The outlook for UK economic growth

remains uncertain, with ongoing pressure driven by the Covid-19 pandemic, our developing trade relationship with the EU

post-Brexit, and expected higher inflation driven by energy prices and supply constraints.

A similar picture exists at a global level where a range of risk drivers continue to sow uncertainty including further Covid

related restrictions, geopolitical risks from protectionist measures, social unrest, the Ukraine conflict, and advanced

economies’ governments’ inability to deliver a significant fiscal stimulus to revive economic growth.

During 2021, we have been cautious in our credit portfolio, focused on consolidating the portfolio into secure assets should

markets become more volatile. We also have extremely limited direct exposure to the crisis in Ukraine, with circa £3 million

from a legacy private equity investment, with a focus on Russia, held in our shareholder assets. We are confident in the

resilience of our portfolio and the situation remains under careful review. In addition, PIC carries out close management of its

balance sheet, and actively hedges its balance sheet against adverse movements in financial markets. PIC monitors areas of

potential pricing bubbles that may see market corrections in order to limit exposures where appropriate. The business holds

a significant amount of risk-based capital to protect against market movements.

Rounding convention

The SFCR is presented in pound sterling rounded to the nearest million which is consistent with the presentation in the IFRS

financial statements. The QRTs are presented in pound sterling rounded to the pound. Rounding differences of +/- one unit

can occur.

A. Business and Performance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202117

B. System of Governance (unaudited)

The below chart shows the Group’s governance structure. Along with other annual reviews of our governance processes,

thestructure is reviewed to make sure that it is fit for purpose and remains as such in the context of the Group’s

growthprospects.

Nomination

Committee

Audit

Committee

Risk

Committee

Investment and

Origination

Committee

Remuneration

Committee

ESG

Committee

Executive

Committee

Management

and Operating

Committees

PICG Board

PIC Board

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202118

B.1 Governance Function

Board of Directors

Pension Insurance Corporation Group Limited

PICG is governed by its Board consisting of 13 directors, 12 of whom are non-executive.

Of the non-executive Board members, two are nominated by Reinet PC Investments (Jersey) Limited which as at

31 December 2021, holds a 49.37% interest in PICG, one is nominated by Luxinva S.A., a wholly owned subsidiary of the

AbuDhabi Investment Authority, which holds a 18.15% interest in PICG, one is nominated by Blue Grass Holdings Limited,

aCVC entity, which holds a 17.37% interest in PICG, and one is nominated by MP 2019 K2 Aggregator, L.P., an HPS Investment

Partners entity, which holds a 10.23% interest in PICG.

The Board maintains overall responsibility for PICG Limited as an entity and an oversight responsibility for the Group to

ensure the Group operates in the best interests of its policyholders, shareholders, employees and other stakeholders.

TheBoard is also responsible for setting the Group’s long-term objectives and commercial strategy.

The main activities of the Group are conducted through its principal operating subsidiary, PIC.

The Board has delegated the day to day management and administration of the Company to the Chief Executive Officer

(“CEO”) who has established the Executive Committee at the operating entity level, PIC, to assist the CEO in day to day

running of PIC.

PICG Board

Director Approved Function

Jon Aisbitt SMF 7 Group Entity Senior Insurance Manager Function

SMF 9 Chairman

Tracy Blackwell SMF 1 Chief Executive Function

SMF 7 Group Entity Senior Insurance Manager Function

Jake Blair SMF 7 Group Entity Senior Insurance Manager Function Appointed 7 June 2021

Judith Eden Non-executive Director

Tim Gallico SMF 7 Group Entity Senior Insurance Manager Function

Julia Goh Non-executive Director Appointed 1 October 2021

Stuart King Non-executive Director

Arno Kitts Non-executive Director

Josua Malherbe SMF 7 Group Entity Senior Insurance Manager Function

Roger Marshall SMF 14 Senior Independent Director

Jérôme Mourgue D’Algue SMF 7 Group Entity Senior Insurance Manager Function

Mark Stephen Non-executive Director

Wilhelm Van Zyl SMF 7 Group Entity Senior Insurance Manager Function

Pension Insurance Corporation plc

PIC is governed by its Board consisting of 14 directors, 12 of whom are non-executive. Seven of PIC’s directors are

independent, including the Chairman.

Of the non-executive Board members, two are appointed by Reinet PC Investments (Jersey) Limited which as at

31 December 2021, indirectly holds a 49.37% interest in PIC, one is appointed by Luxinva S.A., a wholly owned subsidiary of

theAbu Dhabi Investment Authority, which indirectly holds a 18.15% interest in PIC, one is appointed by Blue Grass Holdings

Limited, a CVC entity, which indirectly holds a 17.37% interest in PIC, and one is nominated by MP 2019 K2 Aggregator, L.P.,

anHPS Investment Partners entity, which holds a 10.23% interest in PIC.

The Board has overall responsibility for the operations of PIC and oversees the management of the Company in the best

interests of its policyholders, shareholders, employees and other stakeholders, and to set the Company’s long-term

objectives and commercial strategy.

The Board has delegated responsibility for a number of functions to Board Committees as set out below. The Committees

allhave Terms of Reference setting out in more detail their responsibilities.

B. System of Governance (unaudited) continued

Pension Insurance Corporation Group Limited | Solvency and Financial Condition Report 202119

PIC Board

Director Approved Function

Jon Aisbitt SMF 7 Group Entity Senior Insurance Manager Function

SMF 9 Chairman

SMF13 Chair of the Nomination Committee

Tracy Blackwell SMF 1 Chief Executive Function

SMF 7 Group Entity Senior Insurance Manager Function

Sally Bridgeland SMF 10 Chair of the Risk Committee Board member from 28 January

2021, Chair of Risk Committee

from 11 March 2021

Jake Blair SMF 7 Group Entity Senior Insurance Manager Function Appointed 7 June 2021

Judith Eden SMF 12 Chair of the Remuneration Committee

Julia Goh Non-executive Director Appointed 1 October 2021

Stuart King Non-executive Director

Arno Kitts Non-executive Director

Roger Marshall SMF 11 Chair of the Audit Committee

SMF 14 Senior Independent Director

Jérôme Mourgue D’Algue SMF 7 Group Entity Senior Insurance Manager Function

Peter Rutland SMF 7 Group Entity Senior Insurance Manager Function

Steve Sarjant SMF 10 Chair of the Risk Committee Stepped down as SMF 10 on

10 March 2021. Retired from the

Board on 31 March 2021

Rob Sewell SMF 2 Chief Finance Function Stepped down as SMF 2 and

retired from the Board on

9 December 2021

Mark Stephen Non-executive Director

Wilhelm Van Zyl SMF 7 Group Entity Senior Insurance Manager Function

Dom Veney SMF 2 Chief Finance Function Appointed 10 December 2021

Audit Committee

The Board has established the Committee in fulfilling its responsibilities regarding financial reporting, the effectiveness of

internal controls and risk management systems, processes and compliance matters.

The Audit Committee comprises four independent non-executive directors. The Board is satisfied that members of the Audit

Committee have relevant accounting and financial reporting experience.

The Board has delegated to the Committee the responsibility for overseeing the following key areas:

Financial reporting

Monitoring and, where necessary, challenging the Group’s financial reporting processes including key accounting issues and

judgements as well as methods and assumptions used in the valuation of the technical provisions under Solvency II and

suggested basis including prudential margins for the technical provisions under IFRS.

Reviewing and, where necessary, challenging all material information presented in the Annual Report and Accounts before

these are approved by the Board.

Providing oversight of progress towards implementation of IFRS 17 and the financial impact on the Group’s reporting.